The vision to build a seamless link between healthcare delivery and insurance remains the goal

This is a topic which is of great interest in investing circles – health insurance; however, in order to paint a holistic picture, it has to be seamlessly integrated with healthcare delivery. India is notorious for heavy out-of-pocket expenses and a terribly inefficient claim settlement landscape – out of the USD 110bn+ healthcare market in India, IPD spends would amount to around 40-45% of which only USD 5-6 bn are processed in claims, indicating significant headroom for growth; and despite a large chunk of the market spends in OPD, the OPD insurance piece is completely untapped thus far. One of the major pain points to solve for in order to unlock value here is the claim settlement process – the vision is to make every settlement function and feel like a cashless claim.

Private insurance has been growing at 23-25% CAGR over the last few years – people are solving for distribution; however, the claim settlement piece remains to be solved, but this has to be done in tandem with creating a healthcare delivery network at the back

A healthcare provider network is critical to solving for cashless insurance claims while ensuring standardized healthcare delivery in the process. Patients are plagued with a very stressful journey in settling claims – managing documents, bills, and low visibility across the process. Hospitals need fast claim processing with minimum deductions and also suffer from poor visibility on the TPA process. Insurance companies need a broad healthcare delivery network to increase their premiums and lower operational costs during claim processing which is currently very manual.

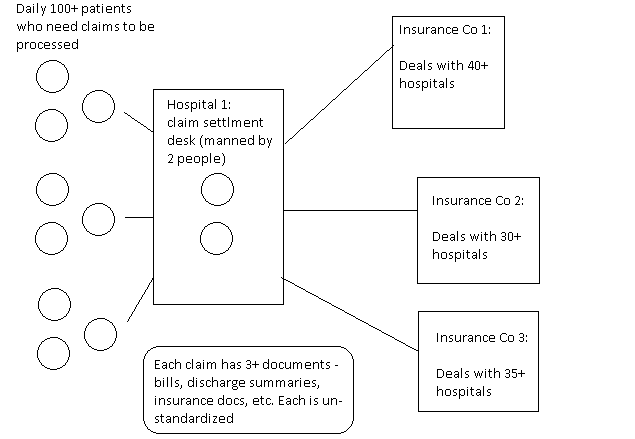

The current workflow in settling claims is severely impaired ->

The TPA desk at any hospital is manned by 1 or 2 people who in turn have to address hundreds of unique claims on a daily basis from the customers/patients and have to coordinate this with 30+ TPAs on the other end with each having their own guidelines. Similarly, Insurance cos and TPAs need to reconcile the billing information, discharge summaries, and insurance documents of different hospitals and process the claims manually – neither the hospitals nor patients have any visibility on which stage the claim is at.

There is an urgent need to solve for an automated claim processing engine with seamless information flow between the different stakeholders on a singular platform -> the patient, the hospital and the insurance company so that TATs in claim settlement can be reduced, deductions can be reduced and a patient can have a seamless experience from hospital selection to discharge, the hospitals can settle claims in a speedy fashion and insurance companies get a strong healthcare delivery network to maximize premiums.

Using technology to integrate hospitals and insurance cos on one platform is very difficult and business model positioning is complex

Since it is clear all three stakeholders need to be integrated on one platform for seamless communication and processing, there arise some critical questions which need to be addressed -> Will the start-up be positioned as a claim processing engine with a network of healthcare delivery providers in the backend and if that is the case, who will the core customer be?

By positioning as a claim processing engine with a network of hospitals at the backend, does the business model build a large enough outcome? The odds are that start-ups will charge a take rate for every claim processed. From our research, this seems to draw anywhere between 2-4% take rates which may limit the size of the opportunity, however, there seems to be a case for generating strong leads for hospitals which convert to procedures/tests for the hospital where an 8%+ take rate might work.

We are looking for companies who have unique insight into cracking the technology integration piece across all the stakeholders

Platformization of the communication and processing of claims seems to be plagued with very high adoption friction across stakeholders. The following become possible channels to drive adoption:

· The insurance companies (and TPAs) themselves –There are a limited number of health insurance providers with even fewer having a high willingness to adopt technology – seems like a tough sell on the legacy players; new age players with a tech DNA might be a low-hanging fruit.

· Hospitals – Will be a tough sell whichever way we look at it, it is common knowledge that changing/upgrading HMS systems in hospitals itself is an uphill task – making it a difficult proposition for new-age tech adoption.

Thinking out of the box to crack technology integration

· HMS systems – Since all data integrations with hospitals need to start from the hospital HMS, another viable option may be to tap into HMS cos – a single HMS provider might have access to 5k-7k hospital beds across different hospitals.

· WhatsApp – With initial indications of health start-ups having demonstrated Whatsapp-first approaches to onboarding and activating doctors, there may be a case for interesting claim processing engines being built atop of Whatsapp in a way which seamlessly connects across all stakeholders

With so many questions and such few answers, we feel putting out our thoughts will help us get some closure on the open questions surrounding a unified healthcare and insurance play.

We are on the lookout for a solution which can be adopted with minimum friction and has a scalable monetization model – if you feel you have cracked/or have insight into a stronger business model, we would love to hear it!