Most D2C founders in India can tell some version of this story. They log into Meesho on a Monday morning to find that the bestselling SKU last quarter is not the one they had been pushing ads behind. They didn’t know it was the bestseller until the dashboard told them. The algorithm had picked it up, decided it looked like the kind of thing a particular cohort of buyers would respond to, and pushed it into millions of feeds. The founder, increasingly, is a passenger on their own business.

That story is the entire shift, in one anecdote. The world is moving quickly from one where humans decide what they want and machines help them find it, to one where machines decide what we want and we cheerfully oblige. If you are building anything that ends in a transaction, this is the single most important trend to internalize this decade.

The shelf is gone

For most of commercial history, consumption had a clean architecture. There was a need (or a manufactured one), a category, a set of brands inside it, and a shelf, real or digital, where you went to compare. You walked into a Big Bazaar, or you typed “running shoes” into Amazon, or you asked a cousin. The mental motion was: I want X, who makes the best X.

That motion is dying. Watch any heavy user of Instagram, Meesho, or YouTube Shorts today. They are not searching. They are scrolling. Things appear. Some of those things get bought. The category, the comparison, the intent, all of it has been hollowed out. The feed is the shelf, the recommendation is the catalogue, and the algorithm is the salesperson who happens to know what the buyer has been doing for the last three years.

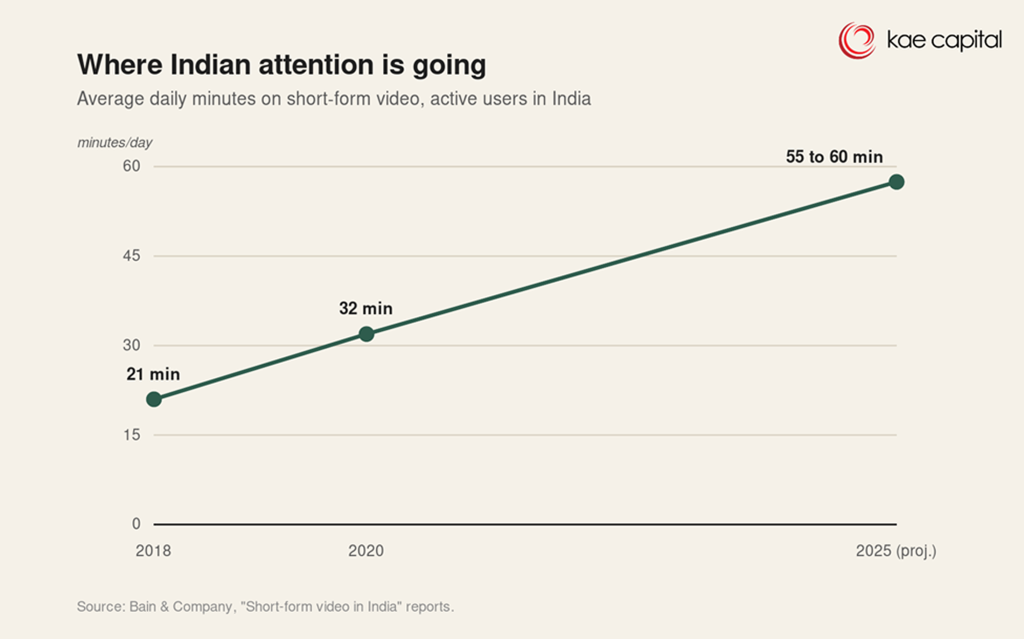

The numbers tell the same story. By Bain’s estimates, India will have 600 to 650 million short-form video consumers in 2025, with active users spending close to an hour a day inside these feeds. Globally, the strongest proof point is TikTok Shop, which is not available in India but is the most useful data point we have for where feed-driven commerce is heading. Its global GMV went from roughly $0.9B in 2021 to $33.2B in 2024 and is on track for around $66B in 2025. That is a 70x jump in four years on a platform that, by design, you cannot search the way you search Amazon. The fastest-growing surface for commerce in the world is one with no shelf at all.

This sounds like a small UX change. It is not. It is a transfer of power.

Intent is the thing being eaten

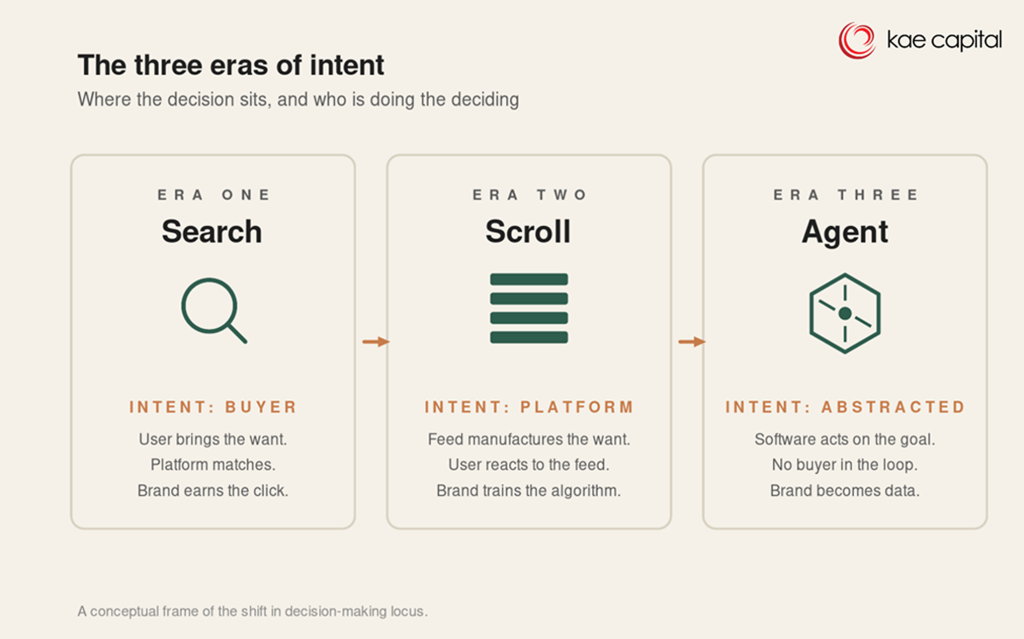

In the search world, intent was customer-side. The user knew what they wanted, and the platform helped match them to it. Google’s whole business is monetizing intent that already exists. Brands paid to be the first answer when someone walked up to the counter.

In the feed world, intent is platform-side. The platform decides what the user should want today, mostly based on what people who look statistically like them wanted yesterday. The user does not bring intent to the screen. The screen manufactures it. This is why so many of the products people now buy are ones they did not know existed twenty minutes earlier, and why nobody can remember a week later what made them click.

The implication for brand building is severe. The old playbook was about owning a piece of mental real estate, so that when intent arrived, you were the first answer. Brands spent a decade making “cola” mean Coke. But if intent itself is being generated inside an algorithm that has no memory of your TV spots, no respect for your shelf placement, and no opinion on your equity, you are not really building a brand anymore. You are training a recommender. The job has changed and most CMOs are still doing the old one.

Taste in the time of feeds

The cultural side of this is stranger than the commercial side. Algorithms were supposed to give everyone a personalized world. In practice, they have made taste both narrower and weirder at the same time.

Narrower because most feeds optimize for engagement, which is a small slice of what humans actually value. Weirder because the feedback loops compound at insane speed. A small group of people develops a niche interest, the algorithm notices, amplifies, mutates, and a few quarters later there is a multi-hundred-million-dollar brand built around something that did not exist a year earlier.

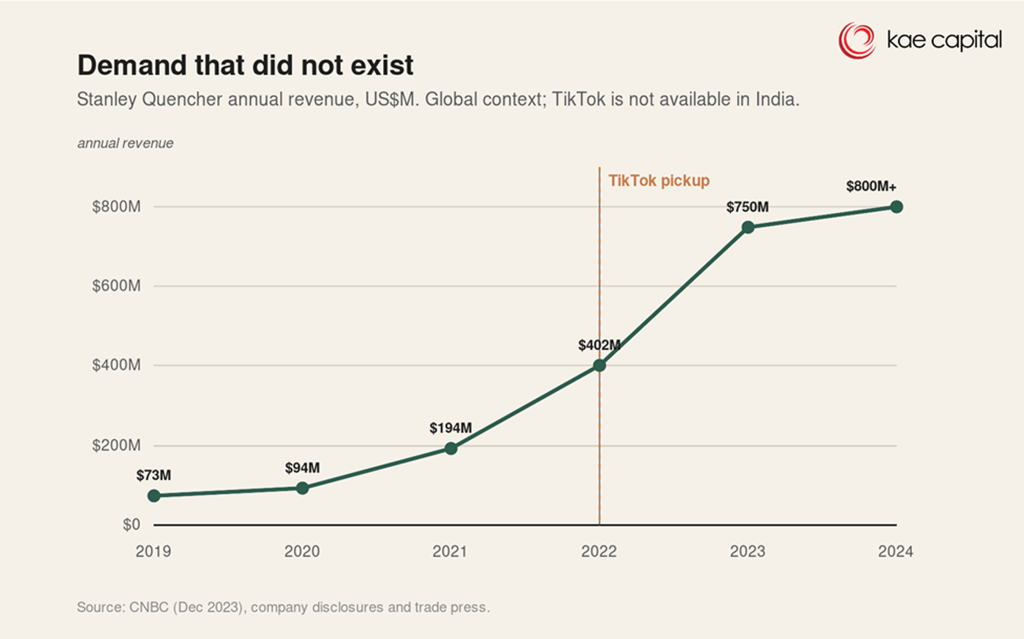

The clearest example is Stanley. The Stanley Quencher cup did $73M in 2019, $94M in 2020, $194M in 2021, $402M in 2022, and around $750M in 2023, largely on the back of TikTok virality. Nobody set out to want a $45 stainless steel cup. The want was assembled, downstream, by a feed. The same playbook is now visible in Indian D2C, where Reels-led brands in skincare, fragrance, snacks, and home goods are scaling from zero to meaningful revenue in twelve to eighteen months, without ever doing a conventional brand campaign.

The more unsettling part is what this is doing to creators, not just to consumers. Listen to almost any chart-topping song today. The hook arrives in the first few seconds. The intro is gone. The chorus is engineered to be loopable in a fifteen-second Reel. This is not an accident. It is what happens when artists, consciously or not, start writing for the algorithm instead of the song. An artist makes a good track. The algorithm picks it up. The artist (and the label) studies what worked, the cut points, the tempo, the lyric that became a meme. The next track is built backward from those signals. Other artists copy what they see working. The recommender, having learned from what it amplified, rewards more of the same. The loop closes. Art drifts downstream of distribution.

The same logic now governs Reels-led D2C. Founders A/B test thumbnails, hook lengths, and product angles not because their customers asked for any of it, but because the algorithm tells them which variant got watched to the end. The customer’s preference and the algorithm’s preference are no longer easy to tell apart, and that is the point.

The Indian wrinkle

The Indian version of this shift has its own shape, and at Kae we think it is the more interesting one.

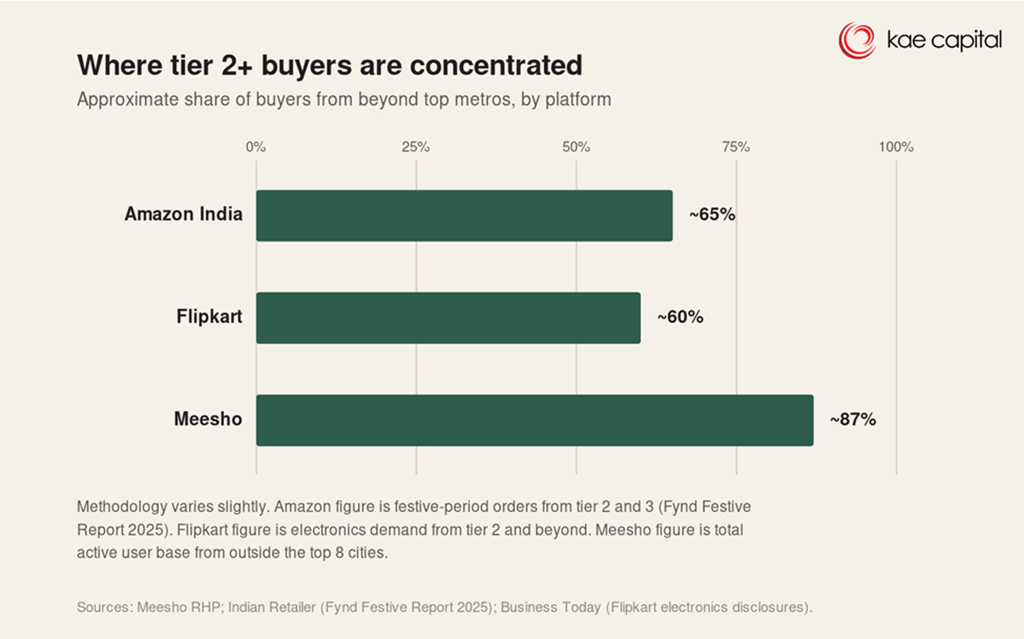

First, voice and video unlock a different consumer. The buyer in Indore or Hubli or Guwahati was never going to type “lightweight breathable kurta for summer” into a search bar. But they will absolutely watch a thirty-second reel of someone showing them one, and click the link in the bio. Meesho today crosses 250M users, with roughly 87% of them coming from outside the top 8 cities. That is not a different funnel for the same customer. It is a different customer who only became reachable because the funnel itself changed.

Second, the platforms with the strongest feeds, Meesho, Instagram, YouTube, Sharechat, do not yet look like the platforms with the strongest carts. The cart is still concentrated on Amazon and Flipkart, where the buyer arrives with intent. Whoever closes the loop between feed-grade discovery and Amazon-grade fulfillment in India builds something enormous. We think the market is one or two product cycles away from someone doing it well.

Third, the brands that win in this environment will not look like the brands that won the last one. They will be faster, weirder, less attached to category orthodoxy, and built by founders who understand that their real competition is not the brand next to them on the shelf, it is the eight seconds before the user scrolls past.

The agent layer is coming

If algorithmic feeds are the present, AI agents are the very near future. Within a couple of years, a meaningful share of routine purchases will be made by software acting on a user’s behalf. Reorders of groceries, replenishment of consumables, travel bookings, basic insurance, utility switches.

The forecasts here are aggressive. Gartner now projects that by 2028, roughly a third of digital user experiences will shift from native apps to agentic front ends, and that on the B2B side, around 90% of buying will be AI-agent intermediated, pushing more than $15 trillion of spend through agent exchanges. Even if you take a heavy discount on those numbers, the direction is unambiguous.

The agent will not scroll, it will not be charmed by a reel, and it will not care about a founder story. This is the second power shift, stacked on the first, and almost nobody in consumer is ready for it. The skills that matter when you are selling to an agent are: structured data, verifiable claims, machine-readable reviews, API-accessible catalogues, and the ability to win on price-quality at the SKU level. Brand equity matters less. Persuasion matters less. Being legible to a model that has been told “find the best one” matters a lot.

If feeds turned brand building into recommender training, agents will turn it into something closer to SEO for machines. The brands that quietly invest in structured product data over the next eighteen months will look prescient by the end of the decade.

What survives

It is tempting to read all this as the end of human choice, which it is not. People are still going to want things, and at least some of those wants will be deep enough to drive search-style behaviour. Higher-consideration categories, luxury, identity goods, things worn in public, things put inside the body, will retain something of the old architecture. The shelf is not dead everywhere.

But the centre of gravity has moved, and it has moved in a direction that almost no one in consumer marketing has fully internalized. The default mode of consumption is becoming passive, ambient, and machine-mediated. The companies that are honest about that will build differently. They will hire data scientists where they used to hire creative directors. They will optimize for the algorithm’s tastes the way they used to optimize for the customer’s. They will accept that the salesperson now lives inside the platform, and the only question is whether it likes their product.

This may very well be the last generation that thinks of itself as choosing. The next one will be chosen for, gently, constantly, and with frightening accuracy. Whether that is a tragedy or just a different way of being a consumer depends on who you ask. At Kae, we mostly care about what gets built next. And what gets built next will be built for the machine first, the human second, and the shelf not at all.