In India, sun exposure is not a lifestyle choice. It is a structural reality.

Large parts of the country sit at a UV index between 7 and 11 for most of the year, firmly in the high to extreme range. Unlike colder or temperate geographies where sunscreen is a summer habit, India experiences sustained UV exposure year round. Add atmospheric haze from pollution and the problem becomes more complex rather than less severe. UVB rays scatter and lose some intensity, but UVA rays penetrate straight through, reaching deeper layers of the skin.

This distinction matters. UVA damage is not immediately visible. It does not always cause redness or burning, but it is responsible for collagen breakdown, pigmentation, premature aging, and deep DNA damage. Multiple studies suggest this damage can begin within 10 to 15 minutes of unprotected exposure. Not hours. Minutes.

Despite this, sunscreen is still treated as an optional cosmetic product rather than what it truly is: the most important intervention for long term skin health in India.

Understanding the problem properly: UVA, UVB, SPF, and PA

Most conversations around sunscreen start and end with SPF numbers. That is part of the problem.

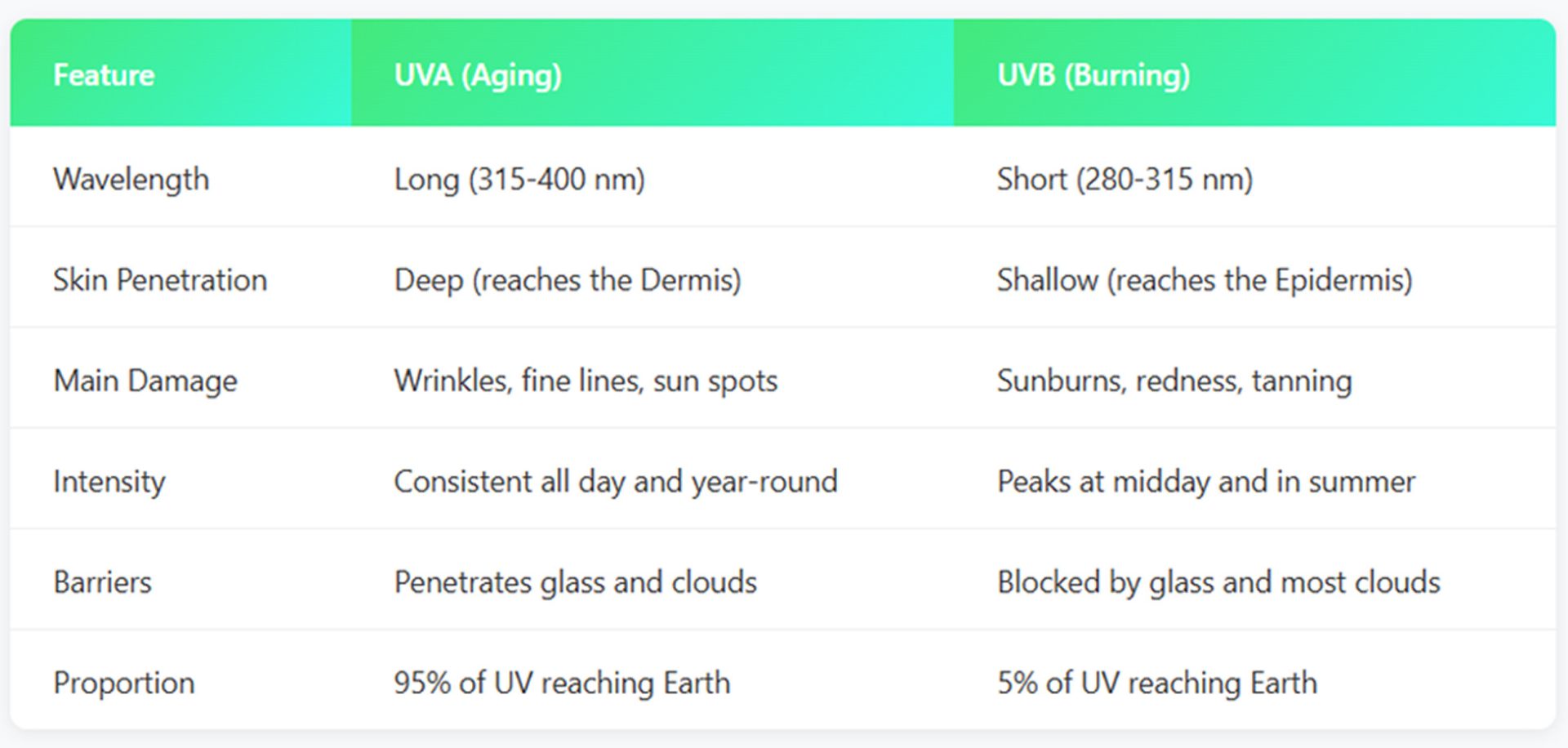

SPF, or Sun Protection Factor, measures protection against UVB rays only. UVB accounts for roughly 5 percent of the ultraviolet radiation that reaches the earth. The remaining 95 percent is UVA, which penetrates deeper into the skin and causes cumulative damage over time.

UVA and UVB behave very differently. UVB peaks around midday, is largely blocked by glass, and causes visible sunburn. UVA is present throughout the day, passes through windows and clouds, and quietly accelerates aging and pigmentation.

This is why SPF alone is an incomplete metric. A sunscreen can have SPF 50 and still offer weak UVA protection if it is poorly formulated.

That does not mean SPF is irrelevant. It needs context.

SPF 50 and above makes sense for people who commute, walk outdoors, or spend long hours outside. SPF 30 and above is acceptable for mostly indoor days. In both cases, the PA rating is critical. PA measures UVA protection. Ideally, consumers should look for PA+++ or PA++++ and broad spectrum coverage should be a baseline expectation, not a bonus.

The melanin myth

There is a persistent belief that Indian skin does not need sunscreen because it is naturally rich in melanin. While melanin does provide some protection, it is roughly equivalent to SPF 13 to 15 at best. That level of protection is inadequate against UVB and offers very limited defense against UVA.

Melanin may delay visible damage, but it does not prevent it. Indian skin still ages, pigments, and accumulates DNA damage, often in ways that are harder to reverse later.

Why Sunscreen matters more than Retinol

Modern skincare culture is dominated by actives. Retinol, acids, peptides, and serums are positioned as transformative, while sunscreen is treated as a necessary but boring step.

From a biological standpoint, this framing is backward.

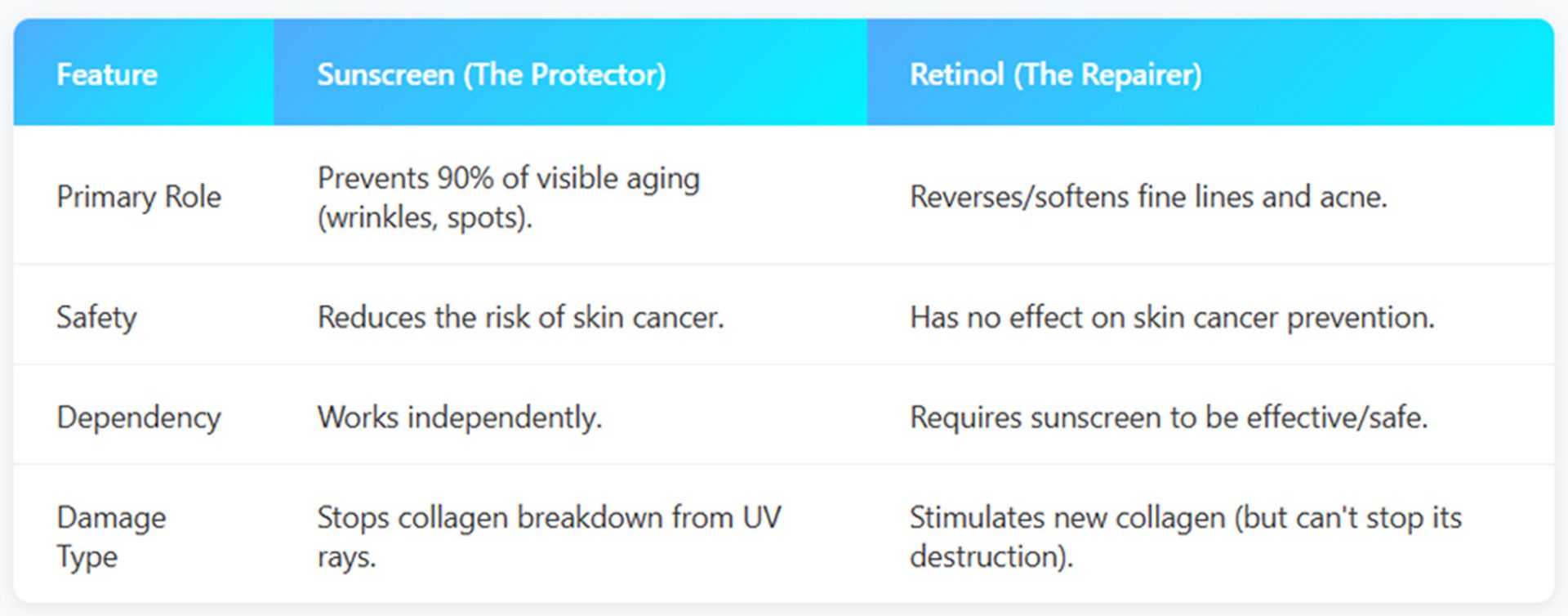

Retinol helps repair some damage after it has occurred. Sunscreen prevents the damage from happening in the first place. Sunscreen reduces collagen breakdown caused by UV exposure. Retinol stimulates collagen production but cannot stop its destruction. Sunscreen lowers the risk of skin cancer. Retinol does not. Retinol also requires consistent sun protection to be used safely and effectively.

If skincare were architecture, retinol would be renovation. Sunscreen would be the foundation. Without it, everything else eventually collapses.

What has changed: Modern sunscreen technology

One reason sunscreen has historically felt unpleasant is that older UV filters were limited. Heavy textures, white cast, greasiness, and instability were common. That constraint no longer exists, at least outside the United States.

Over the last decade, sunscreen technology has advanced significantly, particularly in Europe and parts of Asia.

New generation filters now address gaps that older formulations could not.

Mexoryl 400 covers the ultra long UVA range between 380 and 400 nm, a band closely associated with deep cellular damage and persistent pigmentation. Most traditional sunscreens lose effectiveness around 370 nm.

TriAsorB extends protection into high energy visible blue light, which has been linked to melasma and hyperpigmentation, especially in melanin rich skin.

Bemotrizinol, also known as Tinosorb S, offers exceptional photostability. It does not break down easily in sunlight and helps stabilize other filters. Its expected approval in the US around 2026 represents a long overdue regulatory shift.

Filters such as Uvinul A Plus, Tinosorb M, and Uvinul T 150 have become the global gold standard because they are stable, effective, and less likely to penetrate deeply into the skin.

The irony is that Indian consumers, who arguably need advanced sun protection the most, often either lack access to these technologies or pay a premium for imported products.

Regulation in India is finally catching up

Recent changes by BIS are meaningful because they align sunscreen testing with Indian realities.

In vivo SPF testing is now mandatory. Brands can no longer rely on calculated or purely laboratory based estimates. SPF must be proven on human skin under real conditions using ISO 24444 protocols in Indian labs.

In addition, ITA classification requires testing across a diverse range of Indian skin tones, particularly to substantiate claims like no white cast.

This raises the cost and complexity of building sunscreen, but it also raises trust. The category needed this reset.

What is the gap?

Sunscreen is not a cosmetic add on. It is the most essential part of any skincare routine.

And yet, it is the most skipped.

People will invest time and money into five step serum routines, layering actives carefully and tracking ingredients, only to miss sunscreen entirely. In doing so, they undo most of the benefits they are trying to create. Without sun protection, actives become damage control at best and counterproductive at worst.

Despite this, there are very few brands that have taken on the responsibility of educating consumers properly on sunscreen or innovating meaningfully on how sunscreen fits into daily life.

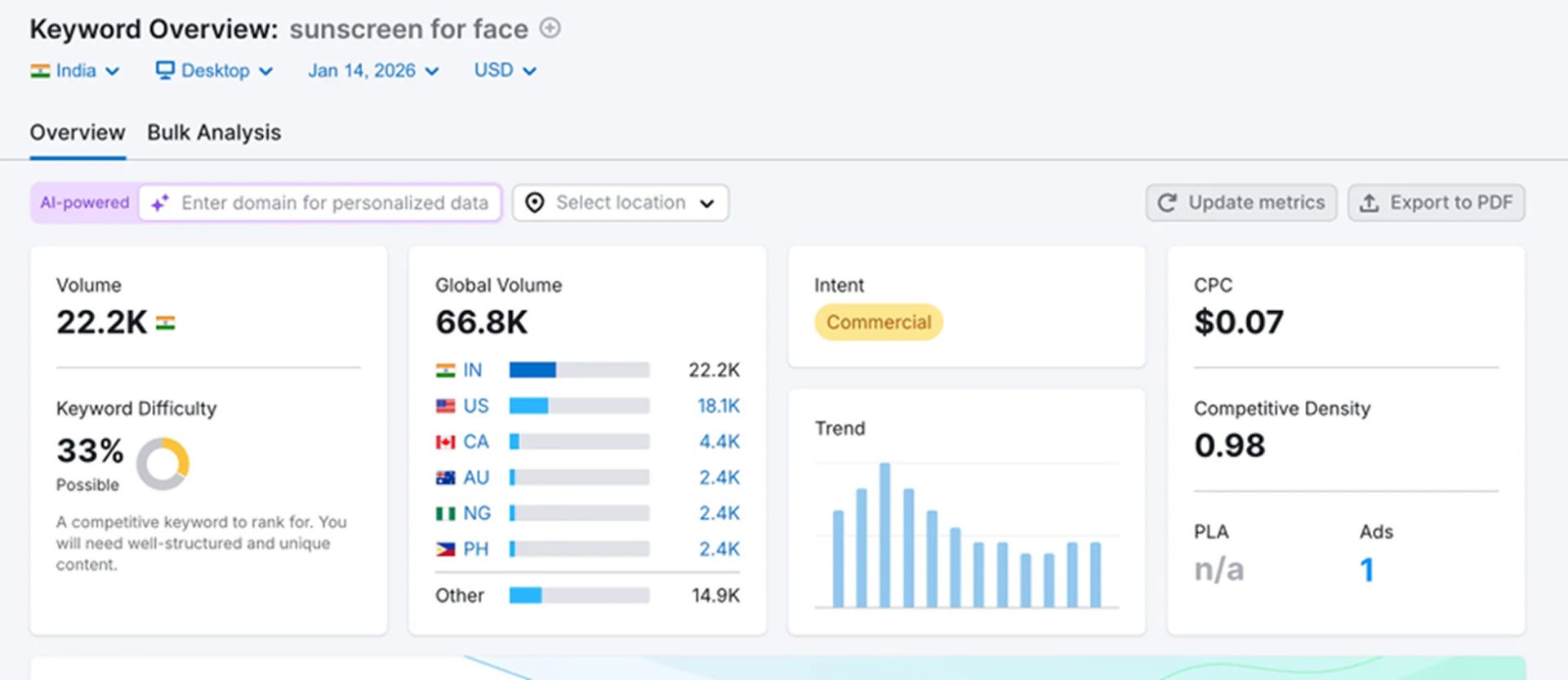

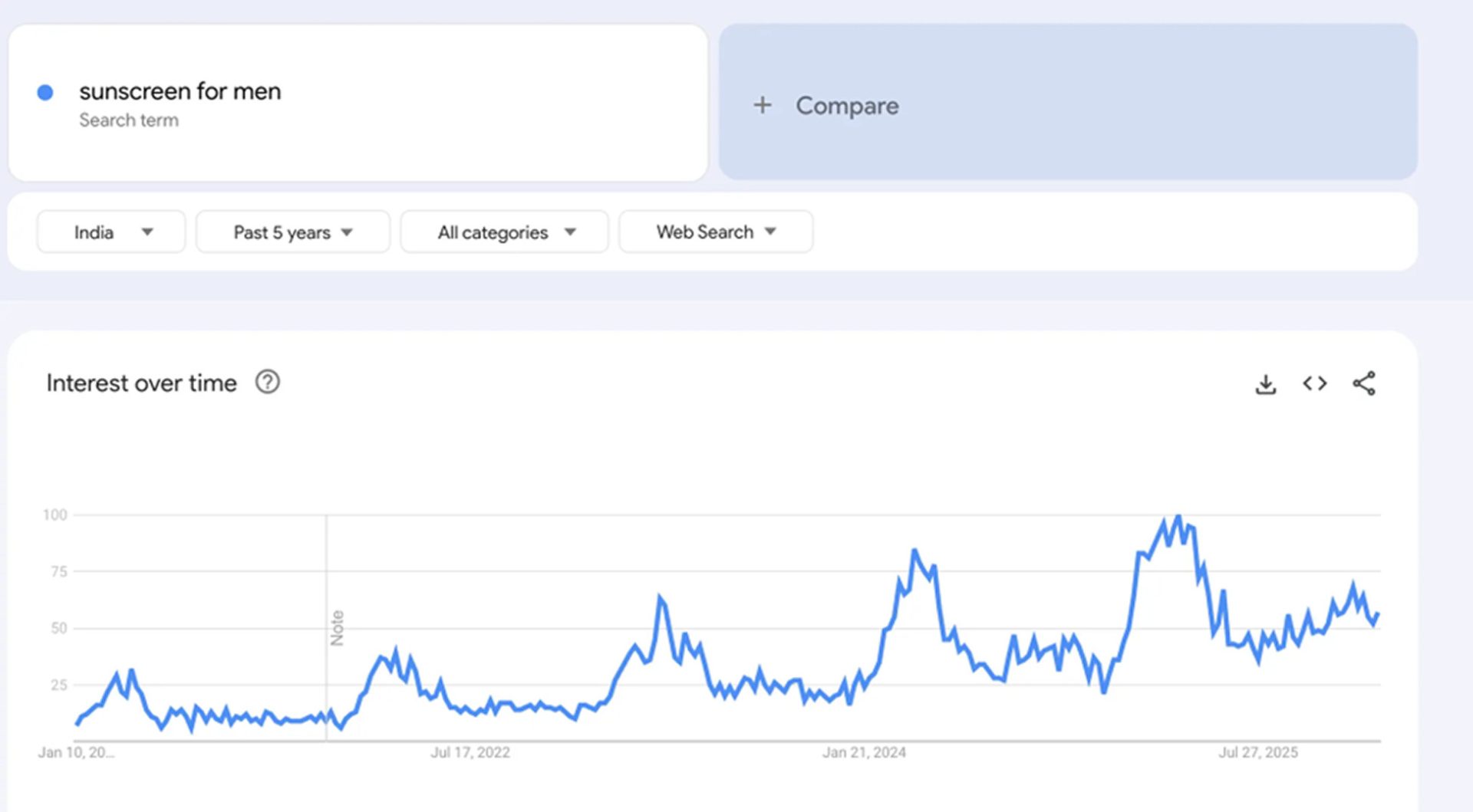

Things are changing rapidly. Search behavior shows that people are no longer looking for a generic sunscreen.

Google trends for sunscreen searches:

They are searching for sunscreens tailored to specific needs such as face use, acne prone skin, men’s formulations, lightweight textures, and no white cast. Consumer intent is fragmenting into use cases, but the category has not evolved at the same pace.

Globally, Korean and Japanese brands have done an excellent job on formulation and texture. However, they are often expensive, imported, and not designed for Indian heat, humidity, or reapplication habits. The sunscreens that truly work and are trusted tend to cost a premium that makes daily, liberal usage difficult.

Indian consumers also expect a lot from their sunscreen. They want it to not pill, to offer strong PA protection, to leave no white cast, to feel lightweight rather than silicone heavy, and to work across different moments of the day. Very few products manage to deliver all of this well.

This is the core gap.

Sun protection is a necessity, not a luxury. Yet the products that do the job properly are often priced, positioned, or designed like indulgences.

The opportunity is not to compete to be someone’s moisturiser, serum, or face wash. It is to become their suncare provider, across formats, use cases, age groups, and skin types.

What consumers are telling us

Consumer behavior around sunscreen has changed significantly.

- First, sunscreen is no longer seen as a luxury. It is increasingly viewed as a basic necessity, particularly among urban consumers.

- Second, sunscreen has taken on a subtle form of signaling. People who reapply sunscreen in public are often perceived as informed, disciplined, and intentional about their health.

- Third, consumers are educated about actives, but many have not internalized one critical truth: actives do not work without sunscreen. This creates a meaningful opportunity for education led brands.

- Fourth, reapplication is fundamentally broken. Creams feel heavy. They disrupt makeup. Sticks often feel unhygienic. Sprays feel unreliable. Even when intent exists, habit fails.

- Finally, sensory experience matters. Heavy or greasy sunscreens create friction. If a product feels like it is sitting on the skin, people simply stop using it. Consistency is everything in sun protection.

How I’d Build a Suncare Brand in India

There is a clear gap in the market for a brand focused purely on sun care. Today, sunscreen is usually just one SKU in an army of serums, face washes, moisturisers, masks, and other verticals.

There are three structural reasons why existing beauty brands will find it hard to fully ride this sunscreen wave.

First, marketing and new product development budgets are spread across all SKUs, not just suncare. Even if a brand launches five different sunscreen variants, the real work lies in educating consumers on choosing the right one. That education requires sustained investment and often gets lost within a broader beauty positioning.

Second, supply chain and SKU management dilute focus. Managing face care, body care, and hair care together makes it difficult to aggressively scale the distribution of a single product line. Sunscreen needs depth across formats and use cases, not just presence.

Third, positioning and trust are hard to realign. Mission led brands like Supergoop! resonate because every single SKU aligns with the same promise of protection. For a beauty brand that has built equity in fast growing categories like serums, pivoting entirely to suncare may not make strategic sense.

This creates room for a brand whose entire identity is built around sun protection.

I believe that five years from now, the suncare section on Nykaa will be significantly larger than it is today and will host large brands doing over 100 crore in annual revenue, dedicated entirely to sun protection.

Product Roadmap

The strategy is to build across real use cases rather than chasing individual ingredients.

The initial lineup includes a basic necessity sunscreen with no white cast, latest generation chemical filters, high absorption, and SPF 50. Pricing is expected at 550 for 100 ml and 380 for 50 ml.

A scalp sunscreen follows, positioned around scalp health and protection. This is an acquisition led product with very little competition in the Indian market.

Reapplication is addressed through a stick format designed specifically for Indian skin tones and climates, priced between 300 and 400.

A body spray sunscreen is also planned, with a whipped formulation explored if regulatory approvals allow.

Subsequent launches include a body oil with SPF, SPF products with skinification benefits, and a liquid chapstick with SPF and plumping agents.

The extended roadmap covers sports specific sweat and water resistant sunscreens, makeup compatible SPF powders and primers, a teen focused sunscreen range, mineral sunscreens for pregnancy and heavy outdoor use, products for bearded men to protect the skin beneath, and SPF infused sun mists designed for travel and leisure.

Once a portfolio of 20 to 25 suncare SKUs is established, the focus shifts heavily toward distribution and marketing. New product development continues, but with a clear goal of staying ahead on filters, textures, and formats so the brand remains the most loved and most used suncare name in India.

Geographic Expansion

The first phase of expansion focuses on the Middle East, including UAE, Saudi Arabia, Jordan, Kuwait, and Qatar. This is followed by Southeast Asia, Europe, and eventually the United States.

Global Benchmarks

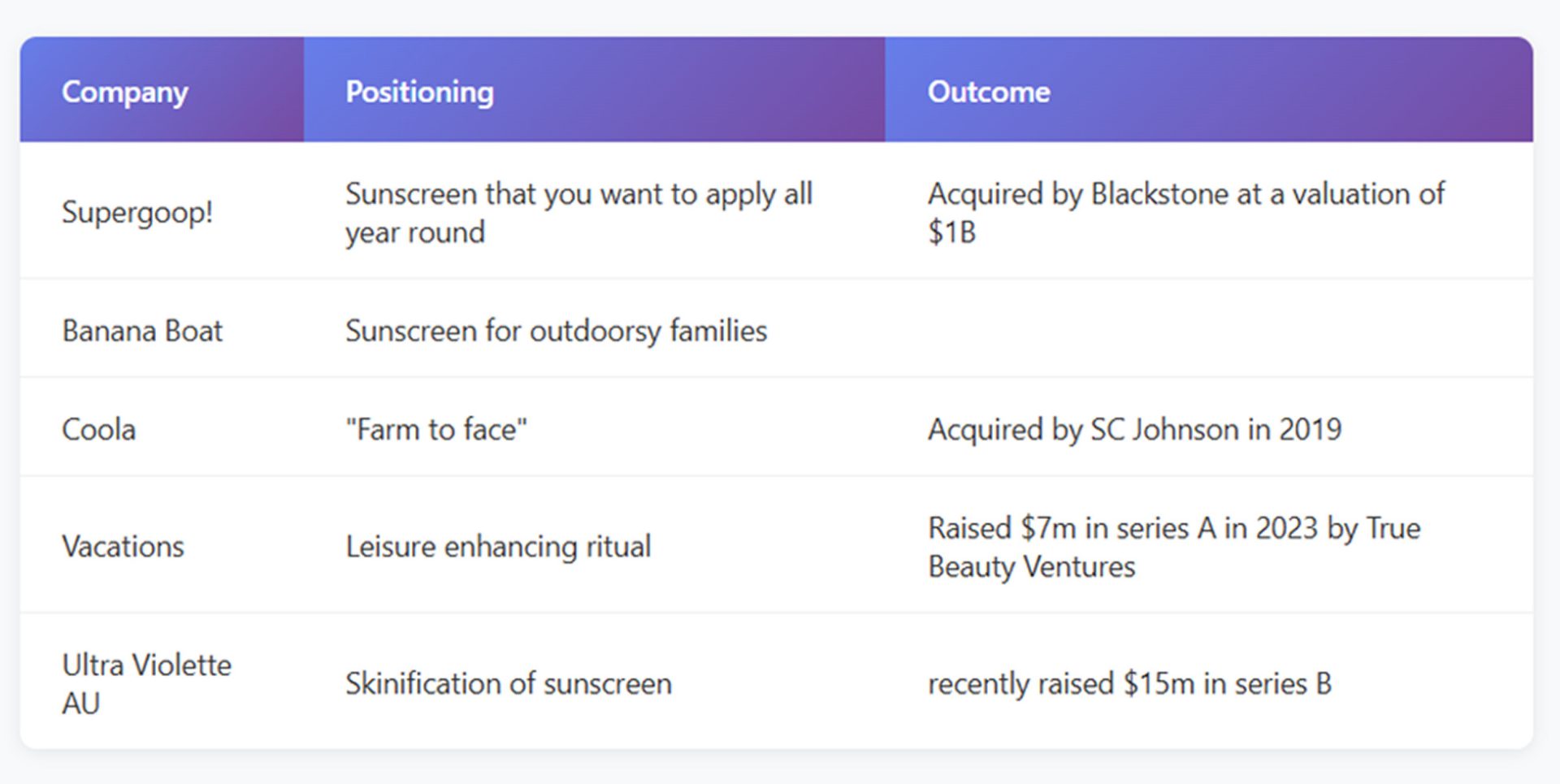

Globally, the playbook is already visible.

Supergoop built a brand around making sunscreen desirable and habitual and was acquired at a billion dollar valuation. Banana Boat owns the outdoor and family segment. Coola positioned itself around farm to face formulations and was acquired by SC Johnson. Vacation reframed sunscreen as a leisure ritual and raised institutional capital. Ultra Violette focused on skinification and built strong momentum in Australia.

The pattern is clear. The brands that win do not treat sunscreen as an accessory. They treat it as the category.

The Takeaway

Sun protection in India is not about vanity or trends. It is about acknowledging environmental reality and responding with products that are effective, comfortable, and easy to use.

Sunscreen is not an add on to skincare. It is the infrastructure that makes skincare work.

The brands that understand this early may look unexciting at first. In hindsight, they will look inevitable.