With over $ 130+ Trillion flowing globally in cross-border volumes, cross-border fintech offers a rare opportunity to create multiple unicorns. 16% of cross-border revenues (not flows) lie in EMEA, 8% in APAC, 5% in LATAM, and 6% in NA (as per EY)

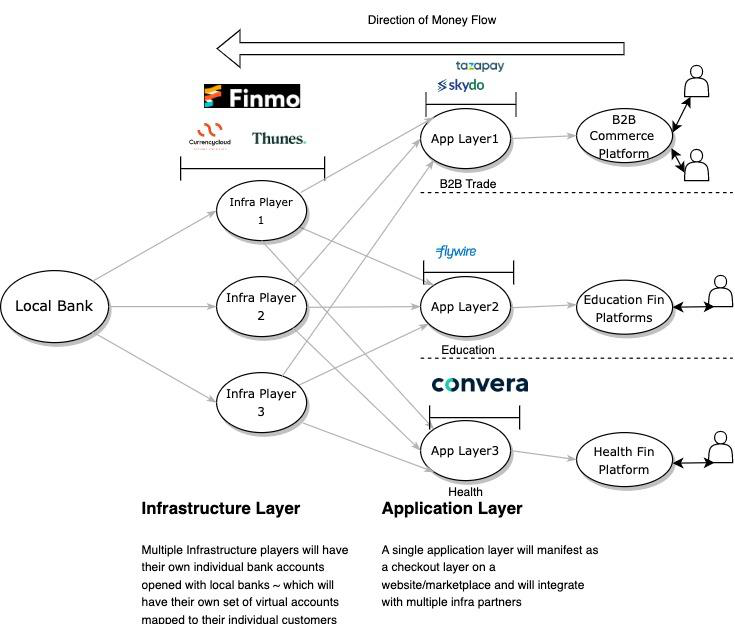

For the purpose of understanding the landscape better, we have divided it into Infrastructure and Application layers

Infrastructure layers help integrate with local banking rails in both/either sender and receiver geographies. They, in turn, integrate with fintechs (Wallet providers for cross-country money transfers, International Money remitters etc.). They solve for:

- Virtual account creation (which in turn helps them access local payment methods & helps with multi-currency accounts creation)

- FX rates by buying and converting currency in bulk

- Reconciliation – This may not be a service offered by all infra players. This depends on the value prop being offered to their customers.

- Take on average 50 bips on GTV

Application layers own the customer, they may manifest as a checkout page on marketplaces:

- They acquire and manage customers

- Solve for customer support and are usually the closest to customers ~ allowing them to build out other higher margin services.

- The take rates here vary depending on the core use case ~ players can make up to 80 bips as checkout solutions, an additional 20 bips as treasury solutions, and potentially upwards of 1% per month as working capital interest on a monthly basis

Bifurcations between Infra and application are not cut and dry, and often there exist fintech players who are infra providers in one geography, and application layers in other geographies. For eg., they may have local bank accounts (i.e. are directly connected to banking rails) in geographies to solve for collections in that geography but need to work with other infra players (who are integrated with the local banking rails in other geographies) to solve for payouts in those geographies.

In India, payment volumes less than $10k fall within the purview of OPGSP and most players solving for payouts/collections within India are operating within the constraints of this license, for volumes in excess of $10k companies are relying on SWIFT-based bank transfers

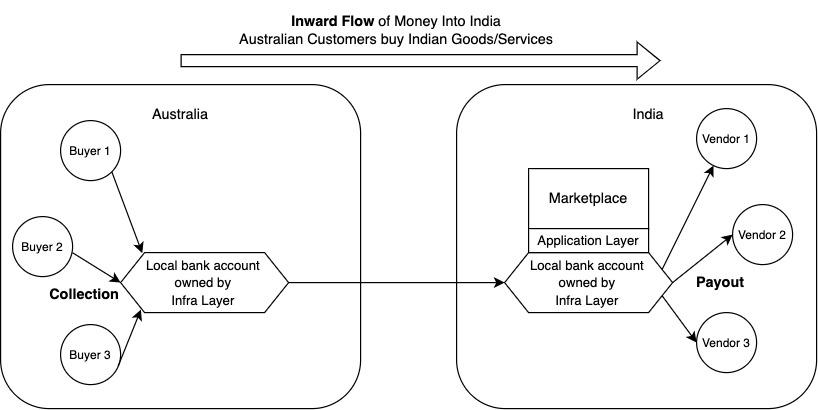

In addition to understanding the value chain, it is pertinent to understand payment flows in a little more detail. Given below is a sample of Inward flow of money from Australia to India ~

Why we choose to make bets in both Infra and Application layers ~

Understanding the market dynamics of payment infra players ~

Infra players will want to have access to as many local bank accounts as possible, and by extension, have access to relevant licenses which allow them the most degrees of freedom, i.e. the ability to send and receive money from multiple geographies. For example, UK’s E-money license (auth. EMI license), Australia’s international remitter license, Singapore’s major payment Institution license, Hong Kong’s Customs and Excise Dept., etc.

There seem to be inherent network effects here, i.e. if I add more geographies solving for both inward and outward payment flow, this will improve the experience of my end customer, i.e., the end customers who will want to send and receive money from as many countries as possible.

Additionally, forex rates are also solved through economies of scale ~ further incentivising market concentration towards only a few infra players.

Having said that, we don’t feel this will be a winner takes all market ~ because each local bank will integrate with multiple infra providers, and we feel that beyond a point forex rates will not be further optimizable, hence commoditizing the FX rates as a differentiator.

So it is our estimate that there can comfortably be more than 3-4 players dominating the global cross-border payment infra market.

With more than USD 130 Trillion flowing through the market, we feel capturing 10 Bn in GTV will ensure a large outcome for us as investors, which we can do by focusing on any one of the several geographic corridors. Additionally, we have seen some infra players start entering the application layer as well.

Understanding the dynamics of Application Layers ~

Infrastructure provides the rails to all kinds of application layers. We can further segment application layers into the following subthemes ~

- Customer segments ~ B2B, B2C, C2C

- Flow of money ~ payouts vs collections

- Use cases ~ B2B trade, health, education, payroll, etc.

Application layers that offer the best customer service/support, and keep expanding their product offerings without compromising on quality will be poised to win. Each use case gives an opportunity to go deeper into specific use cases, for example, education ~ which will allow them to double down on use case specific products like education loans.

We do not think this will be a winner takes all market because there doesn’t seem to be a case for network effects, i.e. the addition of new customers (think marketplaces) will not add additional value to the n+1th customer added on the platform in terms of rates/convenience/etc. Additionally, integration with rails will also not be a differentiator since rails will try and partner with all application layers and we expect this to converge at scale.

We will go after the use cases with the largest TAMs.

Summarizing~

If you are building something in either infra layers or application layers with large vertical TAMs, we would be happy to speak to you!