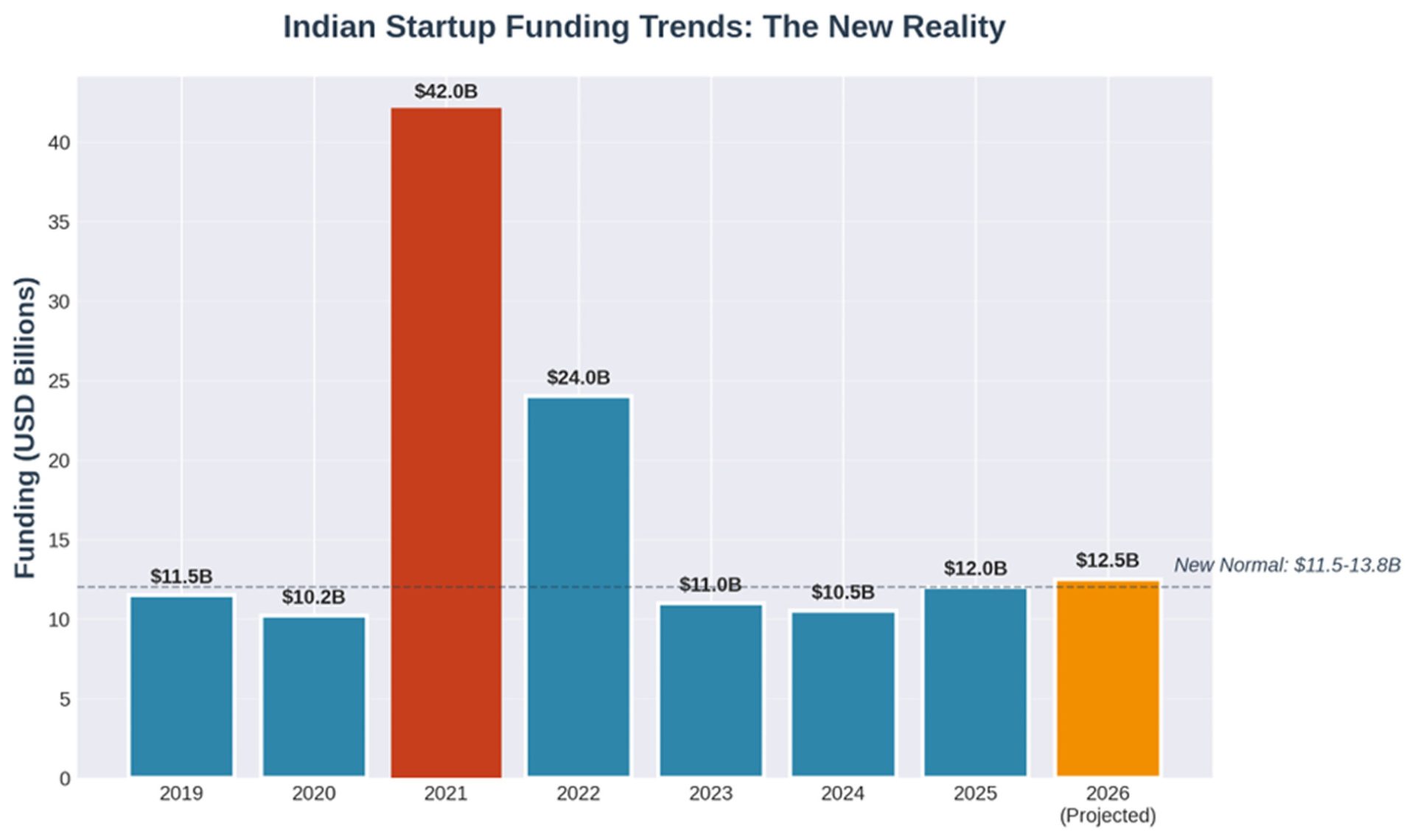

Indian startup funding in 2025 didn’t slow so much as it recalibrated. The numbers tell one story: seed rounds happened, some Series As closed, a handful of growth rounds made headlines. But the texture of those deals tells another. Capital didn’t dry up, it ossified into patterns so rigid that entire categories of founders found themselves suddenly uninvestable, not because their ideas were bad, but because the physics of early-stage financing had fundamentally changed.

This wasn’t a correction. It was a repricing of what “fundable” means.

What Actually Happened in 2025

Capital didn’t get scarce. It got forensic.

The shift in investor diligence between 2022 and 2025 was dramatic. In 2022, companies raised seed rounds on slide decks and Figma prototypes. In 2023, investors wanted early customers and growth charts. By 2025, the bar had moved to cohort retention tables, CAC payback analysis, and gross margin breakdowns at seed stage, not just Series A.

A fintech company in our network raised ₹15 crore in February on ₹35 lakh MRR and what they described as a “strong pipeline.” By October, at ₹1.5 crore MRR after 4xing revenue in eight months, they were passed on by seven funds. The issue wasn’t growth. Their month-3 retention had dropped from 78% to 61%. One fund’s feedback: “Come back when you’ve figured out why customers churn.”

This became the pattern across the ecosystem. Growth without retention was noise. Revenue without margin was a liability. Scale without unit economics signaled a fundamental misunderstanding of business model viability. The capital existed, sitting in funds that had closed large vintages in 2023 and 2024, but the willingness to fund unproven models had evaporated.

Founder behavior bifurcated along adaptation lines.

By mid-year, a clear split emerged in how founders responded to the new market reality. This wasn’t about sector, product category, or founder pedigree. It was about speed of adaptation.

One group cut burn by 30-50% in Q1, sometimes earlier. They pushed break-even timelines forward by 12-18 months, killing features that weren’t converting, letting go of non-performing hires, and ruthlessly prioritizing revenue generation and cost reduction. Customer conversations became weekly or daily, not because a playbook demanded it, but because customer behavior was the only reliable signal. Every rupee was treated as potentially the last.

The other group continued hiring based on the belief that “you can’t cut your way to growth.” They maintained 18-24 month runways assuming Series A would happen on schedule, invested in brand building and team culture, and pitched growth trajectories requiring consistent execution across multiple quarters.

The first group raised their next rounds. The second got bridge rounds at flat or down valuations, burned through those extensions in six months, and either shut down or are still raising on increasingly difficult terms as of early 2026.

The uncomfortable reality: the second group wasn’t operating irrationally. They were following advice that had worked consistently from 2020-2022: build fast, grow faster, address profitability later because scale solves structural problems. This approach didn’t just stop working. It became actively penalized as the market recognized that many high-growth companies from the boom years had destroyed rather than created value.

Founders who updated their mental models in Q1 or Q2 of 2025 adapted successfully. Those waiting for a “return to normal” struggled to survive. The normal they were waiting for isn’t returning.

Series A became a proof point, not a milestone.

Seed funding in 2025 occurred at roughly 2023 volumes, down perhaps 10-15% but not catastrophically. Series A was different. The gap between seed and Series A became the defining characteristic of the funding environment.

Across the ecosystem, roughly 30% of companies attempting Series A raises in 2025 successfully closed rounds. Another 55-60% were still raising as of January 2026, some for nine months or longer. The remaining 10-15% pivoted significantly or wound down.

What separated successful raises from ongoing struggles?

Companies that closed Series A rounds demonstrated either: (a) clear path to profitability within 12 months using current burn rates, backed by improving unit economics data, or (b) net revenue retention above 110% with expanding customer ACVs, meaning their customer base was growing in value faster than churn rates. Not projections or models. Actual cohort data showing the behavior pattern.

Companies still raising often had strong top-line growth, sometimes 30-40% month-on-month in H1. But underneath: retention rates requiring constant new customer acquisition to replace churned revenue, unclear margin structures from incomplete cost accounting, or dependency on paid acquisition that didn’t scale economically.

The investor response wasn’t outright rejection. It was “not yet” and “come back when you’ve proven this works.” In practical terms: “This doesn’t look like a sustainable business model, and we’re not deploying capital to find out.”

Series A stopped being a momentum round rewarding growth. It became a proof-of-business-model round requiring demonstration that the company works as a business, not just as a product with users. If the model didn’t prove out at ₹80 lakh MRR, investors lost confidence it would work at ₹8 crore.

The gap between hype and traction widened significantly.

Categories that attracted attention but struggled to convert interest into funding:

AI copilots claiming to save users “30% time” but unable to quantify what users did with that saved time or demonstrate willingness to pay. Vertical SaaS platforms where the vertical was “Indian SMBs” and the differentiation was “we’re building X for India,” which proved insufficient as a wedge. D2C brands treating Instagram reach as a defensible moat. Crypto projects, for well-documented reasons.

AI companies in H1 consistently showed impressive demos. The technology worked, output quality was compelling. By H2, the critical question shifted: “How many users actively engage 90 days post-signup?” Answers typically ranged from 15-25%, sometimes lower. Novelty effects wore off quickly when workflow integration remained shallow and tools required behavior change rather than fitting existing patterns.

Categories that attracted less attention but demonstrated clearer traction:

Compliance automation saving finance teams 40+ measurable hours monthly on specific tasks like GST reconciliation or TDS filing. B2B infrastructure addressing unglamorous problems like invoice reconciliation, vendor onboarding, or regulatory filing automation. Fintech products with 60%+ attach rates because they integrated into existing workflows rather than requiring adoption of new tools.

One company built software for chartered accountants, automating ITR filing data entry and form generation. They saved CAs approximately 6 hours per client monthly, charged ₹5,000 annually per CA, and achieved 80% annual retention because returning to manual processes became unthinkable after one filing season. They raised ₹12 crore seed in 45 days with multiple competing term sheets.

The pattern: solving acute problems for customers with budget, measuring impact in terms they care about (hours saved, errors reduced, revenue increased), and charging prices representing fractions of delivered value. Companies with these elements raised successfully. Those with “large TAM” and “strong growth” but vague value propositions got exploratory meetings that didn’t convert.

What 2025 Revealed About Early-Stage Dynamics

Burn efficiency emerged as the primary survival predictor.

Analysis of 2022-23 vintage companies revealed a stark pattern: companies successfully raising follow-on rounds weren’t necessarily the fastest growers. They were companies maintaining burn multiples under 2x.

Burn multiple calculation is straightforward: rupees burned to generate one rupee of new ARR. Spending ₹20 lakh to add ₹10 lakh ARR equals a 2x burn multiple. Under 1.5x represents exceptional efficiency. Under 2x is solid. Above 3x is concerning unless growth exceeds 20% month-on-month, and even then represents a precarious runway dynamic.

Companies encountering serious difficulties in 2025 typically had burn multiples above 4x. They were growing, sometimes impressively, but expensively. When they approached investors, the economics suggested multiple additional funding rounds before profitability, and investor appetite for that journey had disappeared.

Successful companies addressed burn in Q1 or Q2, when they still had 18+ months runway and could make deliberate decisions. They didn’t wait for market improvement or assume growth would resolve burn issues. They made necessary cuts to extend runway to 30+ months.

This reflects a structural shift in early-stage durability requirements. High burn only functions when the next round is certain, and 2025 demonstrated nothing is certain. That reality isn’t changing in 2026.

Founder psychology differentiated outcomes more than credentials.

Portfolio analysis comparing McKinsey alumni, IIT/IIM founder pairs, and founders without brand-name credentials revealed counterintuitive results. The credential-heavy group didn’t consistently outperform.

Top performers shared two specific characteristics: unusually high tolerance for difficulty and remarkably low ego attachment to being correct.

The most challenged founders were those with lifetime reinforcement of exceptionalism backed by impressive resumes. They had credentials, networks, and pattern-matching advantages. When market conditions shifted, they maintained pitch narratives instead of iterating models. They interpreted investor feedback as noise from people who “didn’t understand” rather than signals from experienced pattern recognition. They defended strategies in meetings instead of testing whether those strategies still functioned.

Successful founders could acknowledge “this isn’t working, let me try something different” within weeks rather than quarters. They didn’t need to be the most intelligent or credentialed. They needed to learn fastest and defend positions least.

One founder without prior startup experience had run a services business for six years. He launched a SaaS product in March, reached ₹8 lakh MRR by June through intensive effort and a strong initial wedge, then hit a retention wall at 50%. Instead of scaling sales to compensate, he stopped operations and called 40 churned customers over two weeks.

Discovery: he’d been solving the wrong problem. His feature set addressed what he thought was important, but customers churned because the product didn’t solve a different, more fundamental workflow issue. He pivoted the entire feature set in 8 weeks. Retention jumped to 85%. He closed an ₹18 crore Series A in December at valuation reflecting the fixed business model.

This psychology succeeded in 2025: extreme ownership of outcomes, zero defensiveness about errors, and relentless iteration based on actual customer behavior rather than assumptions about what customers should do.

Market size became the least valuable signal in pitch decks.

By April 2025, TAM slides had effectively lost meaning. Not because market size is irrelevant, but because every founder could generate “$10B TAM” figures through combinations of consulting reports, market data, and creative extrapolation. It became a credibility requirement rather than a differentiator.

The more valuable question: “Why will you win your first 100 customers? Not why you might or should, but why you will. What do you know or have that nobody else does?”

Strong founders provided answers rooted in unique insight or unfair access: “Six years in senior operations in this industry, observing this specific value-destroying problem daily.” “My cofounder built this exact workflow at their previous company and understands all the failure points.” “We have proprietary data from our previous business that competitors can’t access without replicating our three-year journey.”

Weak founders answered with capability: “Strong team.” “Execution-focused.” “Move fast and iterate.” These are baseline requirements, not competitive advantages. Everyone claims speed. Everyone believes their team is strong. Generic capability doesn’t create wins.

A healthcare company with a ₹400 crore TAM slide was asked: “Why will doctors adopt your software?” Response: “It’s better than current solutions and costs less.” Follow-up: “What do you know about doctor software adoption behavior that others don’t?” No substantive answer beyond “we’ve talked to some doctors who expressed interest.”

Another healthcare company had a ₹150 crore TAM. Same question about doctor adoption. The founder, a practicing surgeon: “I know the three specific reasons doctors won’t adopt new software regardless of quality: implementation time, data migration complexity, lack of EMR integration. I built around all three from day one. Here’s proof from my pilot with 8 surgeons at two hospitals where we achieved 90% daily active usage within two weeks.”

The difference wasn’t market size or credentials. It was depth of insight about the actual problem and actual customer.

Signals That Became More Predictive

Founders who spoke in business language, not startup jargon.

The most successful fundraises in 2025 came from founders who could explain their businesses in concrete business terms, the language appropriate for explaining P&L to an experienced CFO.

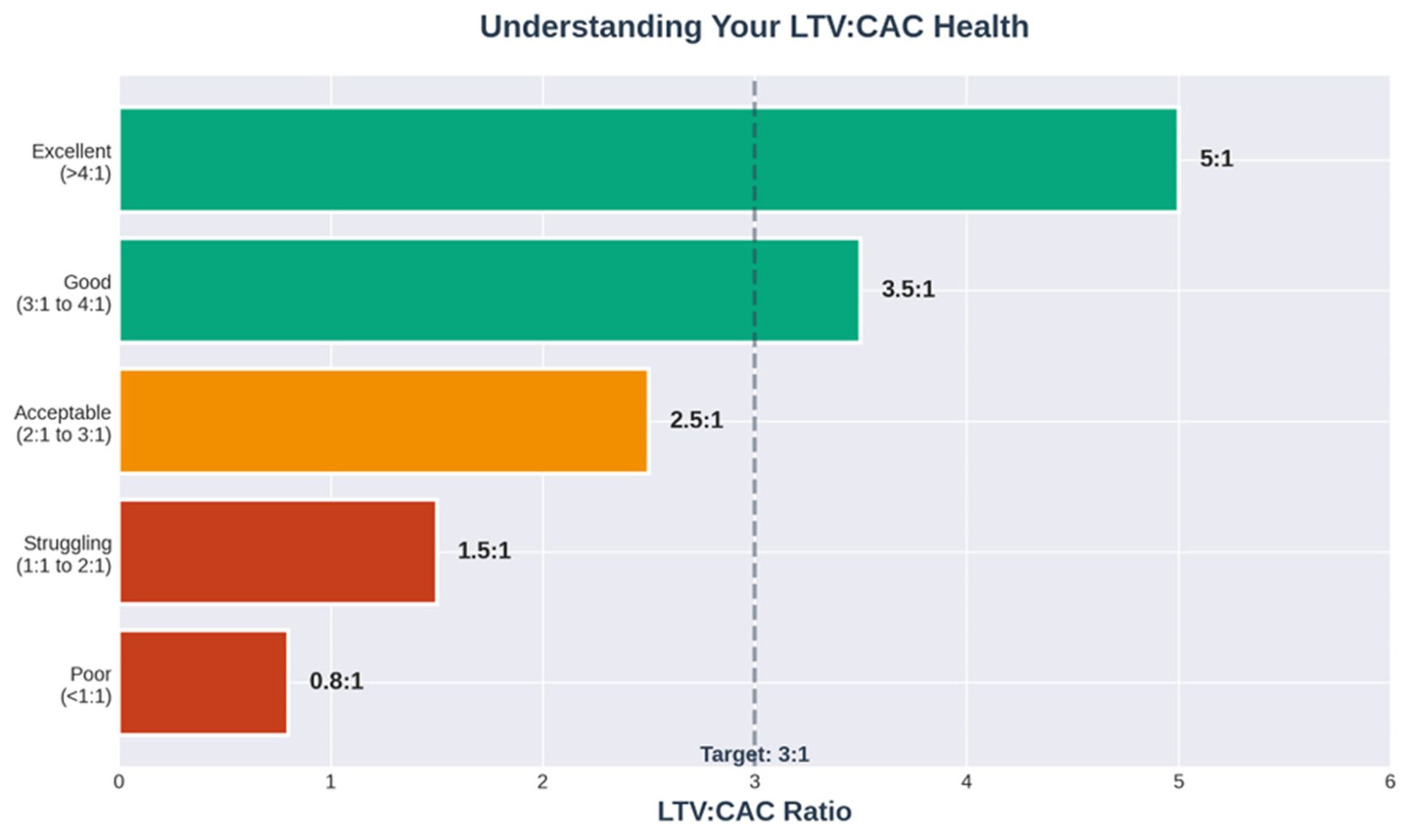

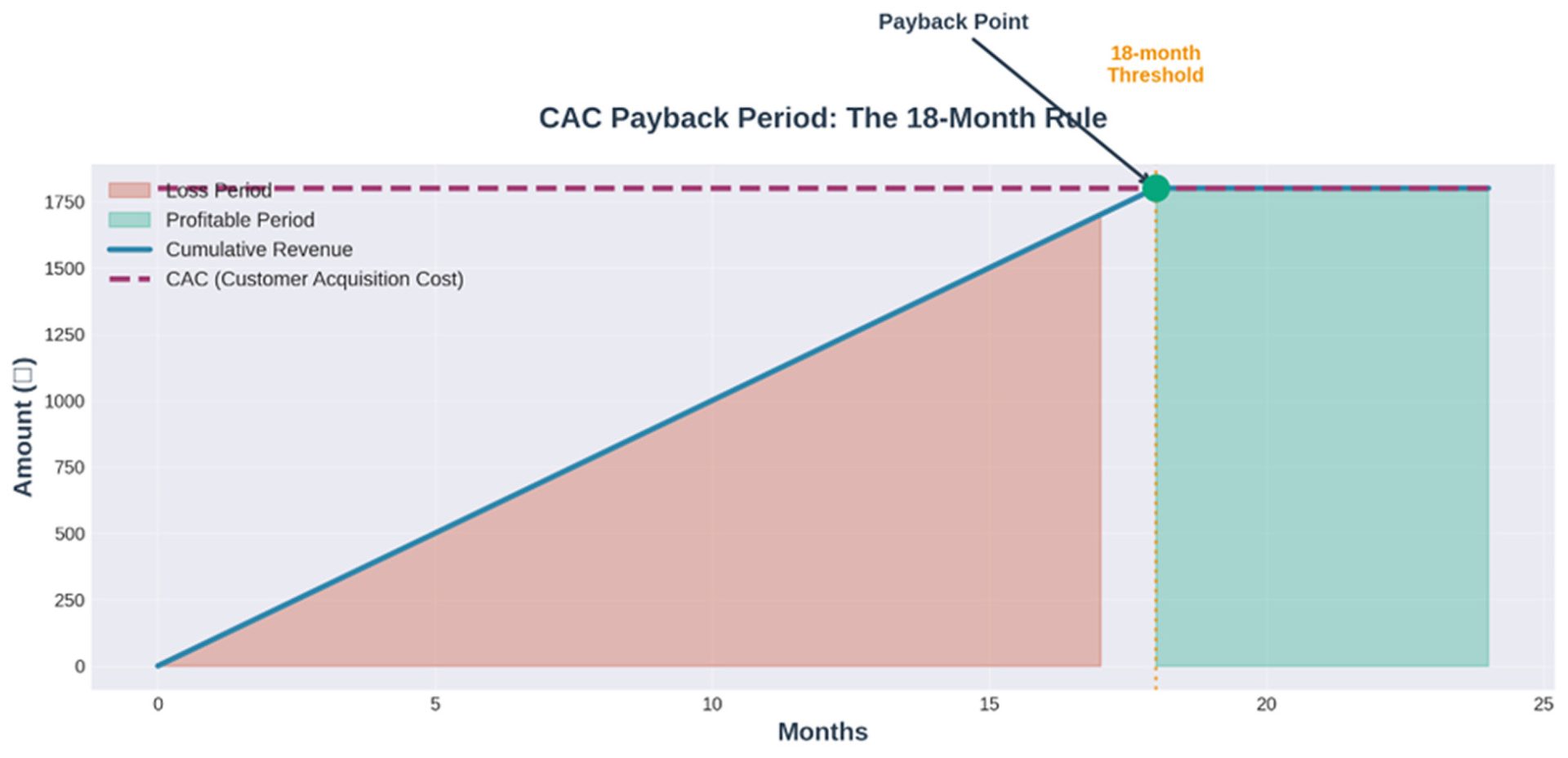

Not: “We have strong unit economics.” But: “Our CAC is ₹8,500, average customer LTV is ₹42,000, we recover CAC in 7 months, and here’s the spreadsheet showing payback by cohort with full methodology.”

Not: “We’re seeing great engagement.” But: “Our DAU/MAU ratio is 38%, average session time is 11 minutes, and our top 20% power users drive 67% of retention and 73% of revenue.”

Investors in 2025 stopped responding to narrative fluency. They wanted operators who understood their own numbers more deeply than the investors asking questions.

An informal test question: “Walk me through exactly how you make money on a single customer, from acquisition through renewal.”

Top quartile responses: Pulling up a clearly frequently-referenced spreadsheet, showing real customer data, explaining margin structure line by line, highlighting exactly where losses occur and why, describing the 2-3 specific levers being pulled to improve economics. Complete explanation in under five minutes with numbers matching the deck.

Bottom quartile responses: “Our LTV:CAC ratio is 3:1” without ability to show calculation methodology. Or calculations using projected LTV based on assumed retention rather than actual retention data. Or omitting major cost categories like customer success, support, or usage-scaling infrastructure costs.

The fundraising outcome gap between these groups approached 100%.

Early signals that actually predicted later success.

Tracking early-stage metrics against companies that raised strong Series A rounds revealed three unexpectedly strong predictors:

Time-to-value under 48 hours. If customers didn’t receive measurable, concrete value within two days of signup, churn rates became catastrophic. Product quality over 90 days was irrelevant if first-use experience didn’t deliver immediate tangible value. Retention collapsed without it.

Best-retention companies had first-session aha moments: “Uploaded invoices and system auto-reconciled 90% against bank statement.” “Connected accounting software and saw 90-day cash flow forecast in 30 seconds.” Value had to be immediate, visible, and relevant to current needs, not quarterly objectives.

Organic expansion within accounts without formal motions. Healthiest-scaling companies didn’t have aggressive upsell playbooks or dedicated expansion CSMs. They had products that naturally spread within organizations. One user invited teammates because tool effectiveness required team usage. One team’s obvious success made other teams curious. Usage grew without sales pressure.

One company averaged 3 seats at customer start, growing to 12 seats within 6 months without outbound effort. When product value is genuinely obvious and workflow integration is tight, it pulls additional users through observed behavior rather than sales pitches.

Weekly shipping cadence without exception. This sounds basic but proved to be the clearest leading indicator. Founders shipping new features, bug fixes, or iterations every single week built dramatically faster feedback loops, learned quicker, caught problems before crises, and maintained velocity that compounded over time.

Monthly or quarterly shippers treated products as finished objects requiring perfection before release. Weekly shippers treated products as living systems requiring continuous improvement based on user behavior learning. Product quality and market fit differences after 12 months were substantial.

Signals that lost predictive value.

“We’re in stealth mode.” Unless building defense technology or working in genuinely regulated spaces where disclosure creates legal risk, stealth mode in 2025 meant: no customers yet and fear of testing assumptions, or overestimation of idea value relative to execution. Neither signals strength.

“We’re a marketplace.” Marketplaces face brutal challenges. Two-sided chicken-and-egg dynamics, low margins, winner-take-all competition, disintermediation vulnerability. The only marketplace successes in 2025 started with one market side and monetized it profitably before adding the second. Building both sides simultaneously from zero almost certainly leads to capital exhaustion.

“Our competitors just raised ₹50 crore.” This became a negative rather than validating signal, typically indicating founders tracking competitor funding rather than customer behavior. The strongest founders rarely mentioned competitors without specific prompting, and when they did, discussed competitor vulnerabilities and mistakes, not funding amounts.

Press coverage. TechCrunch features, Economic Times profiles, Forbes lists stopped correlating with meaningful outcomes. Some best-performing companies had zero press. Some worst-performers had extensive coverage. Press is a lagging hype indicator, not a leading substance indicator.

What Stopped Working

The generous free tier playbook.

From 2019-2022, this strategy worked well: provide genuinely useful free product, hook users on workflow, convert 3-5% to paid over time, expand paid users through additional features and seats. Notion, Slack, Figma and others executed this successfully.

For new companies in 2025, this approach largely failed.

The problem: conversion rates collapsed. Users became comfortable on permanent free tiers, and paid tiers didn’t offer sufficient differentiated value to justify switching. Free versions had improved, often through competitive pressure, making marginal paid value too low.

Multiple companies with 50,000+ free users saw sub-2% paid conversion despite optimization attempts across pricing, packaging, and feature gating. When free tier limits were reduced to force conversion, users churned to competitors rather than converting.

2025 successes either started with paid-from-day-one models or used extremely limited free trials (7-14 days maximum). They forced value conversations during trial periods instead of hoping for organic future conversion. If customers wouldn’t pay after two weeks of full product access, they likely never would. Immediate clarity proved valuable.

Community-led growth without monetization clarity.

Community-as-GTM became popular in 2021-22. Discord servers with thousands of members, active Slack groups, monthly meetups and virtual events, newsletter audiences in tens of thousands. The theory: build trust and affinity, establish thought leadership, then monetize through products or services.

2025 was when “later” arrived, and most communities couldn’t monetize without community destruction.

High engagement existed. Brand affinity was strong. Net Promoter Scores exceeded 70. But monetization requests felt like betrayal to many members: “You built this as a free resource and now you’re charging?” The transaction violated implicit social contracts.

Exceptions were communities built around professional development or B2B networking where paid access was explicit from day one. One finance leader community charged ₹15,000 annual membership, had 400 paying members generating ₹60 lakh ARR from access alone plus additional revenue from workshops and job listings. But they started paid. No free member conversion was attempted because free members never existed.

The “raise big, hire fast” seed approach.

2021-22 conventional wisdom: raise large seed, hire strong team quickly, move fast to capture market opportunity. The assumption: Series A would happen in 12-18 months regardless, so optimize for speed and momentum, not capital efficiency.

This advice probably destroyed more companies in 2025 than any other single piece of boom-era conventional wisdom.

At least 8 companies across the ecosystem raised ₹3-5 crore seeds, hired 12-18 people within six months, burned ₹25-35 lakh monthly, and exhausted runway at 15-18 months without Series A traction. The issue wasn’t hire quality or team talent. It was burn rate relative to product-market fit progress.

At ₹30 lakh monthly burn, companies need to add at least ₹15 lakh new ARR monthly just to maintain reasonable burn multiples. Most weren’t close. They burned capital on team salaries, office space, and overhead while still figuring out basic product-market fit questions. By the time model problems became clear, they had 4-6 months runway and teams they couldn’t afford.

Survivors stayed lean until revenue absolutely justified headcount. Five highly productive people who understood the mission and moved fast consistently beat fifteen people with unclear mandates and overlapping responsibilities.

How 2026 Looks From Here

Early-stage has become more legible, reducing uncertainty.

Entering 2026, the market has strange clarity. The rules are obvious: control burn rate religiously, show repeatable revenue with strong unit economics, prove customer retention, achieve default alive status or demonstrate credible 12-month path to it.

These aren’t new rules. They’re decades-old principles that applied before the 2020-2022 period. For three years, they were optional. Growth covered everything. Narrative justified anything. Capital felt infinite, making mistakes cheap and allowing slow figuring-out processes.

That world is gone. 2026 isn’t the bubble’s return. It’s continuation and solidification of the new normal that emerged in 2025.

Counterintuitively, this makes early-stage investing less risky, not more.

When everyone raises on vision, market size, and growth projections, determining reality becomes genuinely impossible. Every deck looks similar. Every founder has the same market opportunity and unique approach story. Signal and noise become indistinguishable. When only companies with real traction and disciplined operations can raise, signal becomes dramatically cleaner. Businesses can be evaluated instead of narratives. Outcomes can be underwritten instead of potential guessed.

Founders self-selecting into 2026 raises will be those who’ve already done the hard work of model validation. This alone considerably improves odds.

Fewer raises, better survival rates.

Seed volume is expected to drop another 10-15% in 2026 versus 2025. Not from capital scarcity or lack of investor activity, but because founders unable to meet the new standards won’t attempt raises. They’ll bootstrap longer, pivot to different models, or recognize earlier that ideas aren’t working and shut down before burning 18 months and reputations.

Early 2026 is already showing a pattern: companies entering initial meetings have dramatically higher quality than early 2025. Founders arrive with revenue, real retention data, customer references willing to take calls, and specific capital deployment plans. They’ve proven significant model elements before fundraising begins.

Companies raising in 2026 will have meaningfully better fundamentals, tighter operations, more realistic growth plans, and longer runways before needing follow-on capital. Fewer will die in the Series A valley that consumed many 2021-2023 vintage companies.

2018-2019 vintages had strong survival because founders built in disciplined markets where capital was selective and standards high. 2021-2022 vintages had brutal survival because discipline was optional and decks alone could raise capital. 2025-2026 vintages will resemble 2018-2019. This is unambiguously positive for founders and investors, even if it feels harder in the moment.

Decision velocity is increasing in both directions.

A dynamic already evident in deal flow: investors were burned by 2022-23 vintages. They waited too long to pass on marginal deals, gave excessive benefit of doubt to founders with strong narratives but weak metrics, and ended up with zombie portfolio companies that couldn’t raise follow-on capital, couldn’t generate sufficient independent revenue, and couldn’t pivot effectively.

This experience created new investor behavior patterns: much faster decisions both ways.

Founders with genuinely strong traction and clean metrics should expect term sheets in 2-3 weeks, sometimes faster. Investors actively seek deals looking fundamentally different from recent batches. With 80%+ cohort retention, sub-2x burn multiple, and credible winning narratives, funds move extremely fast to avoid losing deals to other investors. Competition for the best deals is arguably higher than 2022, just for far fewer companies.

Founders without traction or with unclear metrics should expect first or second meeting passes. Investors aren’t doing courtesy follow-ups. They’re not “staying close” to watch development. They’re making binary calls quickly and moving on. This feels harsh but benefits everyone. Founders get clear signals faster instead of wasting months on investors who were never going to commit.

Investment focus: infrastructure over disruption.

Infrastructure making existing businesses measurably more efficient. Not disruptive innovation requiring world transformation. Incremental automation fitting existing workflows. Tools compressing 6-hour manual processes to 30 minutes. Software integrating with existing ERPs, CRMs, and accounting systems without expensive implementation or behavior change requirements.

Indian businesses across sectors have critical workflows held together by Excel, WhatsApp, and manual data entry. Founders who can eliminate these bottlenecks, prove functionality, and charge fractions of delivered value have businesses worth backing.

Vertical tools with immediate, measurable ROI customers can self-calculate. Products with value propositions like: “Use this for one month, save ₹50,000 in measurable time or cost, pay us ₹8,000.” Clean input-output. No hand-waving about long-term strategic value or platform plays. Simply: here’s the problem, here’s our solution, here’s exactly what it’s worth in rupees.

Founders who’ve personally lived problems for 5+ years minimum. The best 2026-backed companies will come from founders not discovering problems through market research. They’re solving problems after years of direct experience. They’ve felt the pain, worked around it with temporary solutions, and understand exactly why existing approaches fail. They have domain authority that can’t be Googled or learned through customer interviews.

Areas of caution: scale-dependent models.

Consumer social products. The attention economy is saturated. Distribution is expensive. Monetization is extraordinarily difficult. Risk-adjusted returns aren’t there for early-stage investors unless companies arrive with millions of organic users and clear profitable monetization evidence.

Marketplaces without genuine supply-side lock-in. If suppliers can easily multi-home across your platform and three competitors simultaneously, there’s no moat. It’s a lead generation business with thin margins and constant price competition vulnerability.

Models requiring massive user scale before functionality. The “build audience first, figure out monetization later” playbook is dead. If profitability paths require 500,000 users first without explanation of how to reach 500,000 profitably, expect immediate passes.

Important but non-urgent problems. Founders often want to solve significant societal problems: climate resilience, education access, healthcare affordability. These genuinely matter. But if customers don’t feel acute pain today and don’t have allocated budget this quarter, sales cycles will kill companies before achieving meaningful scale. The focus is on urgent problems with attached budget, not important problems requiring customer education and behavior change.