The Indian e-commerce landscape has witnessed multiple changes over the last decade. While back in the early 2010s, most Indian consumers were only getting acclimated to the idea of e-retail, today the skepticism has given way to widespread adoption. It was in 2020, when the pandemic marked a true inflection point for e-retail adoption, where we saw a surge in online usage. From online food delivery to quick commerce, a new form of commerce was set afoot, and today, we cannot imagine a world without being able to purchase anything digitally.

There are over 230M Indian online shoppers spread across diverse segments. A large part of Indian shoppers come from Tier 2+ cities and GenZ has become a key micro-segment. Multiple factors such as rising internet penetration due to access to cheap data, high smartphone penetration and increasing per capita GDP have all been drivers of this e-commerce surge.

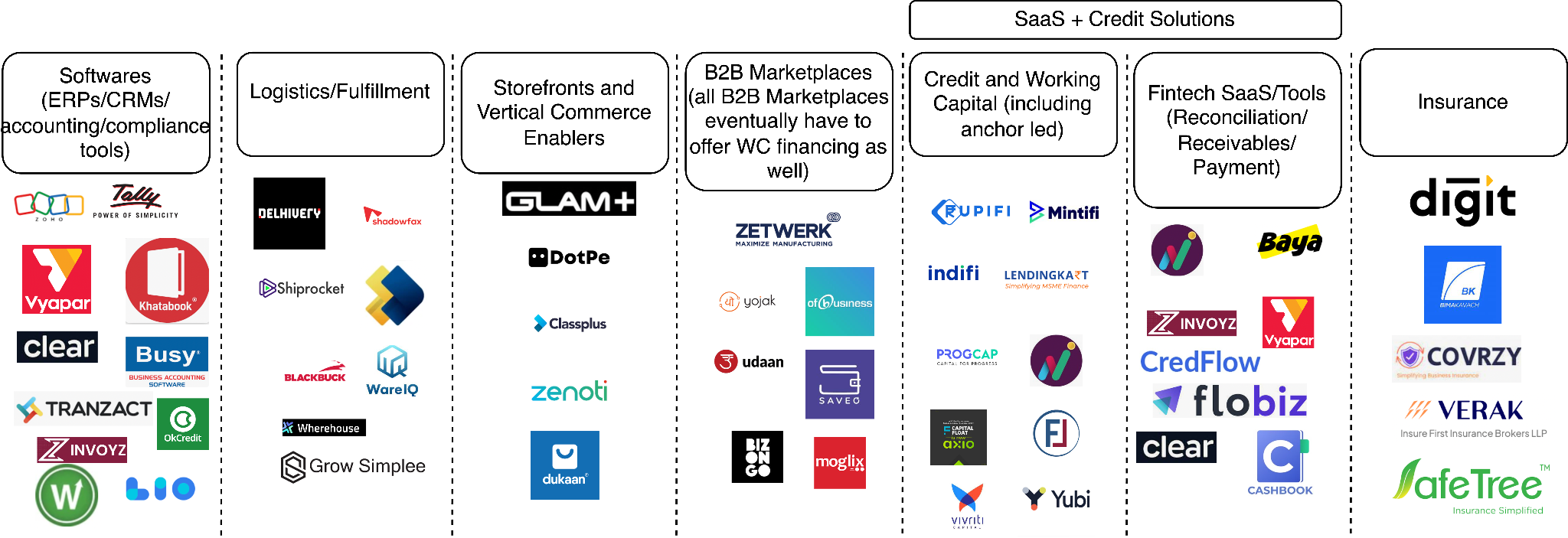

While the story above looks good and e-commerce penetration in India has been on an uptick, it remains relatively low when compared to other countries. Online spending in India is 5-6% of total retail, while it’s 25% in USA and 35% in China. This shows the massive headroom for growth. To fuel this growth, a new age of startups has cropped up known as e-commerce enablers. They are a form of service providers that mitigate the inefficiencies in the current e-commerce landscape and improve the potential that can be achieved. India will need models that help businesses scale, and cater to the varying needs of its diverse shopper base – with different price sensitivities, language requirements, quality expectations and delivery timelines.

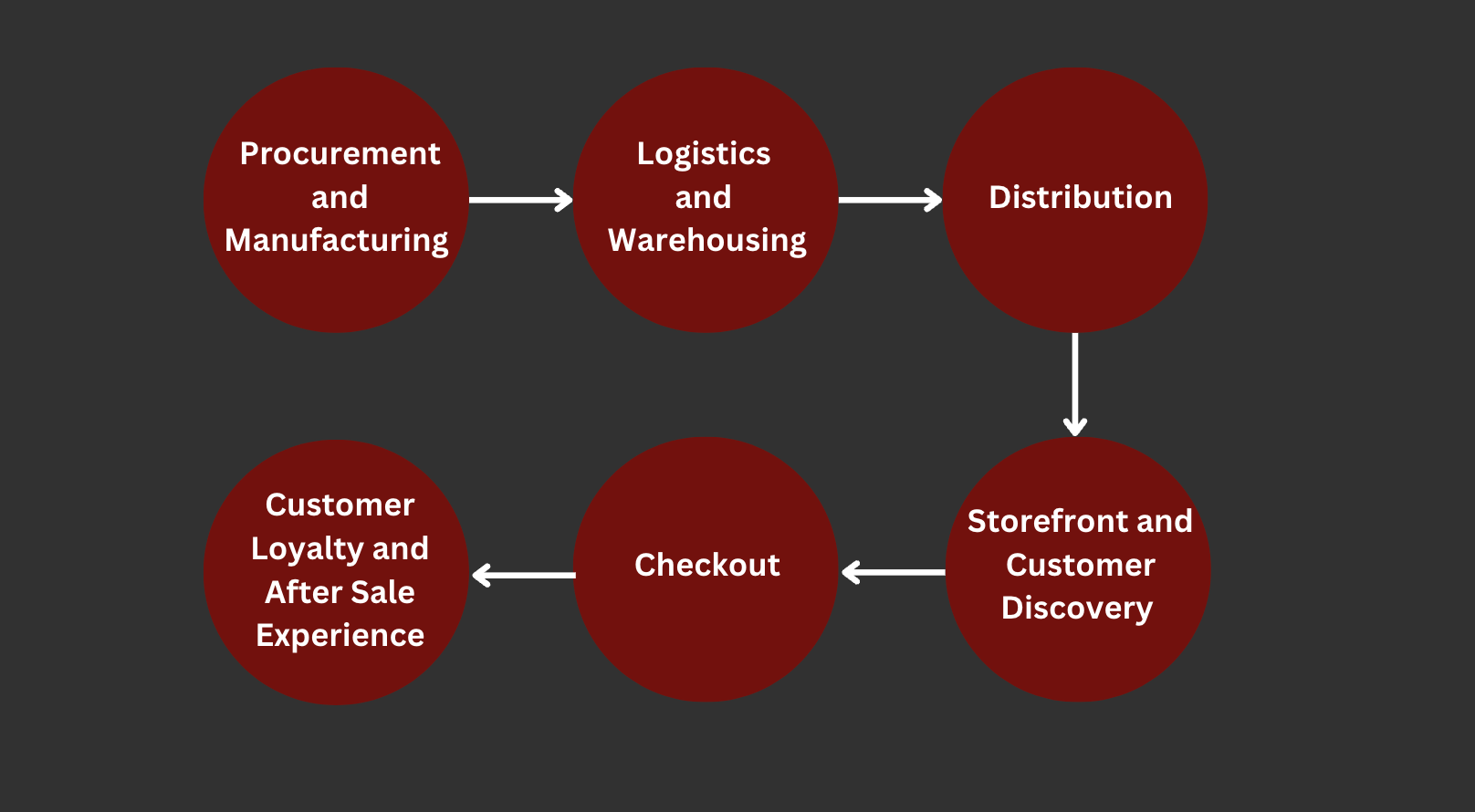

If we look at the entire value chain from the procurement of raw materials until the product reaches the consumer, multiple checkpoints and stakeholders are involved. Below is a brief visual of the value chain.

In this blog, we dive deeper into 2 parts of the value chain – manufacturing and distribution

Manufacturing

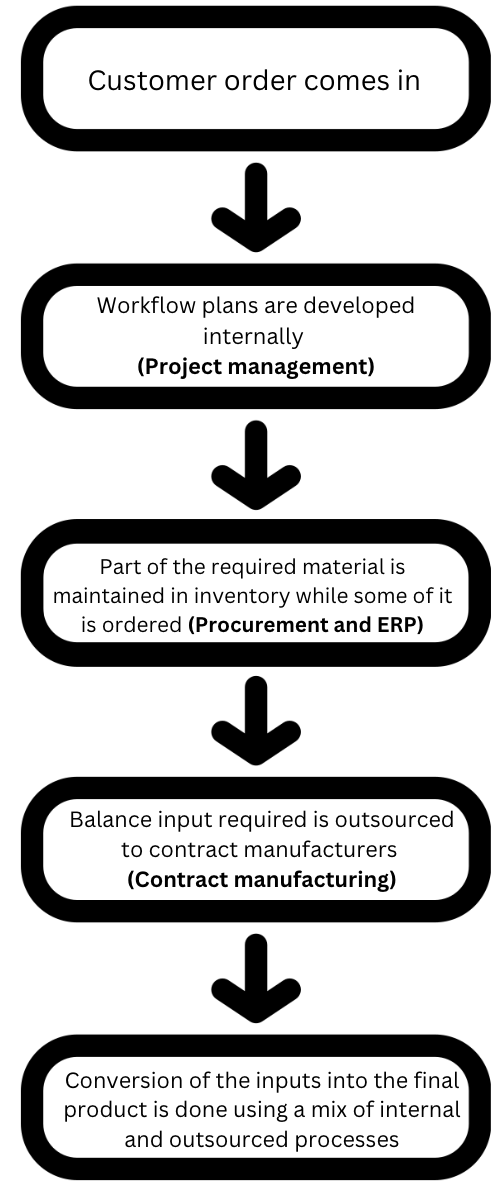

Manufacturing is the first step in the supply chain.

The need: Gone are the days when large segments of the population were making do with brands that were available at the nearest store. The segmentation was mostly done on price points and it was a distribution-led era. Today, Indian consumers comprise more granular segments, each with its own preferences. Over the last few years, there has been and will continue to be a proliferation of brands to cater to such segments that are primarily online first. These brands will be at a relatively smaller scale and will need more agile and responsive manufacturing facilities; that can offer good quality products at low (minimum order quantity) MOQs, at low cost and quick turnaround time (TAT). In addition, global commerce has become more decentralized and countries look at different hubs to source and manufacture critical components.

Where we are: While the Indian manufacturing industry has been growing quickly and is amidst rapid transformation, there are still multiple points of friction that persist. The manufacturing sector contributes ~5% to the GDP and India’s export contribution to global trade is only 1.6%. While the government has been pushing to revitalize the sector with initiatives for what is known as modern manufacturing, the infrastructure around it remains mired in the industrial age. However, with multiple tailwinds, India has an opportunity to emerge as a global manufacturing hub; not only are multiple Indian companies looking at manufacturing in their homeland but also international companies are shifting their manufacturing bases here. Electronics manufacturing could expand by 21% to touch $604B by 2032.

The gaps: Many manufacturers still rely on old technology and traditional production methods that lead to inefficient production processes. Most new-age D2C brands require agile manufacturing, with small batches to meet constantly changing consumer preferences and in order to keep up with a highly competitive landscape. Production methods are capex intensive, and to cover costs, manufacturers operate with high volumes, while brands have to struggle to deal with high inventory and long working capital cycles. Outdated machinery and high dependence on manual labour lead to delayed production timelines and inconsistent quality. Limited use of modern technology inhibits the manufacturers from adequate resource planning, monitoring machinery utilisation or inventory planning. This results in longer lead time and therefore lost sales / high inventory for their customers (brands). These are only a few of the multiple bottlenecks that prevent the manufacturing sector from operating productively.

Emerging whitespaces: Today, primary innovation has been on different modes of mechanization and automation. A convergence of digital, biological, and physical innovations, is transforming the entire value chain. It integrates digital technologies like IIoT, AI, cloud computing, advanced industrial robotics and 3D printing with various sectors, enhancing on-ground manufacturing, quality management, supply chain, maintenance, and customer service. These changes in the manufacturing sector have also been tagged under the next revolution of Industry 5.0.

We have identified various segments within the manufacturing value chain that have seen innovation over the last few years and will continue to do so:

- Capacity utilisation: Technologies that increase the efficiency of the factory operations and maximise resources at hand such as digital assembly mechanisation, AI-powered process controls, remote production optimisation, energy consumption prediction and collaborative robotics.

- Capacity maintenance: Real-time asset monitoring and predictive maintenance to ensure timely maintenance and repair for the long-term durability of factory equipment and machinery.

- Quality Management: IOT-led quality management to bring about standardisation within quicker timelines.

- Capacity modernisation: New form of manufacturing such as on-demand manufacturing, with lower MOQs and precision machinery to ensure capacity efficiency.

- Automated designing and product development: Predictive analytics for product demand, AI-enabled designing, cobot-led product development for sampling and resource planning

- Automated fulfilment support: Predictive planning for warehousing and logistics, delivery vendor network management.

We have had the opportunity to speak to different startups across this space such as startups building nano factories with production bots to industrial software providers using AI and IOT devices. We have understood that there is a large scope to optimize manufacturing functions, enabling the factories to build for India and the world. However, few challenges remain around being able to build large outcomes, as key stakeholders in the manufacturing industry are often reluctant to adopt new technologies. We are hopeful that the multiple tailwinds such as high computational connectivity, government-led initiatives, and the influx of AI-ML technologies make it the correct time to build and solve for the inefficiencies in the sector. While it may be a challenging sector to enter, identifying a relevant problem and building with a clear GTM will allow for a compelling new-age startup.

Distribution

The need: Over the past decade, e-commerce has grown from a niche market to a global powerhouse, reshaping traditional distribution strategies and blurring the lines between online and offline retail. As businesses learn to navigate this e-commerce revolution, they must adapt and embrace the changing dynamics of distribution. While multiple start-ups have been set up across various segments of the logistics industry from aggregator to last-mile delivery, in this blog, we focus on the transition between offline and online distribution.

Where are we: The India logistics and distribution market is huge and has undergone significant transformation over the years. Boom of e-commerce, government reforms, changing consumer preferences and evolving tech infrastructure have been propellers of this change. India’s logistics sector would expand at a CAGR of 10%+, from $200 billion in early 2020 to at least $320 billion in 2025. While till a few years back, most distribution channels were offline, it was during the pandemic the different channels of facilitating e-retail took shape. However, today, most businesses are recognizing that customers not only shop online but also want the experience of “touch and feel”. Many online first brands are exploring the offline route. The likes of BigBasket, Lenskart, Nykaa, and MamaEarth have redirected their efforts towards offline channels in a significant departure from their established digital dominance.

The gaps: Offline presence is not merely about brick-and-mortar stores, but also about personalised experiences to their customers. However, strategically establishing their offline presence either via owned stores or shop-in-shop experiences, online-first brands are trying to navigate this new territory. Offline distribution is expensive and brands struggle with successfully identifying the correct distributor, their sales channels, and retailer outlets. Large brands such HUL or P&G have the scale to work with individual distributors and can dictate their final outcome regarding which retailers they want to sell at. However, smaller brands with less than INR 100 crore in revenue have lesser negotiating power and the end-to-end operating costs to get distribution can be as high as 35-50% of their revenue. Getting efficacy from their sales force to get the retailers to stock products and manage the sales force churn are other major issues. Further, there is a demand generation problem, as fighting for visibility in a new environment where there are no targeted advertisements as in the digital world, becomes tough.

Retailers on the other hand have low bargaining power and are left at the hands of the distributors in deciding what products to keep in stores and the amount of inventory to stock. Additionally, the Indian retailer landscape has also evolved – from small brick-and-mortar stores to modern shopping malls, brands can choose multiple avenues to reach their customers. Innovative formats like hypermarkets, luxury boutiques, and shop-in-shop have also gained popularity, further enriching the offline shopping experience.

Emerging whitespaces: Here we have identified a few spaces we feel have the potential to solve for:

- Access to new brands for retailers: Allows brands to discover new retailers and even allows access to niche retailers in new geographies. These platforms which work with multiple brands can often club the distribution channels for different brands and help brands select the right retailers thereby reducing costs and achieving higher margins. However, churn of brands may be a potential challenge.

- Listing on demand platforms (ONDC): Brands can take advantage of listing through ONDC distributors, especially for products with high AOV and high frequency .

- Additional services: Other services for brands such as payment reconciliation, surplus product disposal, store set-up for modern trade, and improvement of footfall conversion to name a few

- Hyperlocal delivery: As a form of replacement for local retailers. Many players have entered this space, especially focusing on grocery.

We have spoken to multiple startups in the aforementioned segments. There have been platforms that look at facilitating brands setting up shop-in-shop outlets and upselling their products, as well as startups that help create SKU bundles and sell the entire basket of products to retailers. While some might focus on a particular segment such as electronics or only T2+ cities, some are more widespread and look at an array of product types or geographies. While building out an early-stage startup in this space, it is key to not only help brands expand their offline presence, reduce inventory held and thereby bring down their distribution costs, but also help with additional services such as vendor management, GNR generation, payment reconciliation etc. Further, the team needs to have strong ops experience and a clear GTM strategy to be able to execute correctly.

Our view

We at Kae, are bullish about the e-commerce enabler system and feel there is vast potential that lies beneath it to tap. With the advent of online marketplaces, mobile shopping apps, and secure payment gateways, consumers have been provided with unprecedented access to a vast array of products and services from the comfort of their homes or on the go. The change has been nothing short of remarkable and has given a host of opportunities for other new-age exciting startups to be created.

We will follow this up with more blogs that trace the development of other enablers along the product value chain. If you’re building in this space, feel free to reach out to me at urvashi@kae-capital.com