We at Kae are bullish about women’s health and feel large companies can be built out of India.

Women’s health is a pressing need in the Indian healthcare market

It is no secret that the Indian healthcare infrastructure is broken – issues include poor doctor-to-patient ratios, low healthcare/GDP spending, and poor geographic and cost accessibility across the board. These problems further complicate matters for the very critical, yet underserved women of the Indian population.

There is a pressing need for women-centric solutions across multiple verticals like nutrition, sexual and reproductive health, dermatology, and mental health, with existing legacy alternatives being subpar on multiple fronts – stigma, lack of personalized care and outcome-driven thinking have created a gaping trust void.

Why now? – Women’s health stands out as an opportunity to build loyalty through online communities

Over the last few years, women have increasingly come to rely on online channels for most of their health needs as is indicated by the sharp rise in in-bound queries (>100% YoY increase) on both Practo and Google.

All the urban women we spoke to rely on a set of digital communities for their personal health needs – and there has been an increase in the number of such groups in recent times – the plethora of new WhatsApp and Instagram groups are testament to the inherent virality that women’s communities have.

The TAM is large enough to capture the value and build out a venture-scalable business

As VC investors we are on the constant lookout for large monetizable spaces – so it is critical to target those TGs which have a consistent spending capacity with the right hook.

Much like other Indian consumer markets – the majority of the paying capacity lies in Metros and Tier-1 cities. Basis our own research by speaking to potential customers and founders alike – there exists a very high willingness to pay – with the minimum ticket size going upwards of INR 1k per month on average. Our confidence lies in the precedence of women paying periodically for both products – like pads and consumables as well as much higher ticket size procedures and services like laser hair removal, which generates a semi-annual spend of around INR 50k+ easily. Many of the recurring spending categories are must-haves for women.

Most tech solutions today are community and content led, with a paid conversion to a full stack primary care and telemedicine/teleconsult layer with products/tests or procedures on the back to monetize – we believe a sustainable business model in currently available tech platforms will be built on the back of an e-commerce platform to maximise for spend per acquired customer.

We believe the market is ripe to crack the right core customer and hit product and channel fit

The personas in this market are large enough to build out a scalable business – be it a working professional, a homemaker or student to hit PMF. High NPS and customer delight are all about solving for the best value proposition/solution for your niche and this is a question which is very much open to debate with no wrong or right answers.

The niche here we believe will depend on the stage of life the customer is in, and we believe the best way is to look at it as follows –

• 25-35 – issues may range from PCOS, irregular periods, skin and hair, etc.

• 35-45 – issues may be pregnancy-focused, fertility-related, etc.

• >45 – issues may be around menopause, skin, etc.

For each phase of life, the core hooks may vary – from dermatology to reproductive health and fertility; this a question we would love for entrepreneurs to answer!

We are looking for a team that can crack the “trust” factor

Our belief is that unfair advantages will be built around trust and brand recall– most solutions in the market today are still fairly early in their journeys and are on the lookout for weak signals of a potential hockey-stick growth going forward built on deep engagement. We are actively on the lookout for teams with the best insight into building high-engagement communities.

If you have unique customer insight and demonstrated engagement/early indicators of engagement and are confident or even have the slightest inkling that you have cracked or are on route to cracking a scaleable trust-building playbook while offering personalised and empathetic solutions in a standardized manner – we would absolutely, positively love to hear from you – please do write to sarthak@kae-capital.com.

The history of e-commerce is intertwined with the history and boom of online marketplaces. Using technology to connect buyers with sellers and efficiently facilitate transactions, these online marketplaces have overcome the limitations of an offline market. In an offline world, transactions are limited by geographical reach/information asymmetry and are facilitated by intermediaries, online marketplaces however opens a broader market for the buyers and sellers to meet and transact. Marketplaces also have been a go-to model for tech entrepreneurs and investors because if executed well, they have inherent structural advantages to create a large scale and unlock huge values. Some of the most successful innovative businesses of the last few decades have been online marketplaces.

Consumer marketplaces (B2C) have been around for quite some time and have gone through multiple evolutions of business models, starting from listing-focused classifieds, they evolved into transactional ‘open’ and ‘managed’ marketplaces. While we have large horizontal marketplaces like amazon where you can find anything, we also have vertical marketplaces for a specific categories like fashion, furniture, makeup, etc. Now as a consumer, we have an efficient way of buying almost everything online.

While B2C marketplaces have evolved, innovated, and have become ubiquitous in a consumer’s life, the same can’t be said about B2B. In most economies, B2B transactions usually gross up much more than B2C as every supply chain has multiple businesses in between a producer and a consumer. Unlike B2C where the transactions are usually for personal consumptions, here the purchase is typically part of a chain and the cost of delay or quality failure can be very high. Most industries have complex supply chains, low transparencies, and rely on inefficient intermediaries for trust. B2B transactions happen in different value chains/supply lanes wherein the dynamics and participants don’t usually overlap. Inefficiencies in the value chains make sure that there is a very strong case for efficient B2B marketplaces.

The Indian Landscape

India presents an even more interesting landscape. We are an economy of small businesses. 99% of Indian businesses are what is classified as a ‘micro’ business. These firms are usually ‘family’ or ‘single person’ owned, have very few employees, and turnovers in the range of a few crores of rupees per annum. Most of these micro-businesses have poor margins/efficiencies and also have low levels of technology adoption. While these small businesses are millions in number, they contribute to about 30% of the Indian GDP resulting in smaller throughput. Being largely a fragmented market dotted with millions of suppliers and buyers transacting largely in localized markets, India represents a strong case for B2B marketplaces to disrupt the traditional procurement models. Recent changes like GST, digital penetration, and a generational shift can prove to be tailwinds for this.

All market(place)s are not equal

B2B marketplaces have not always worked out. For every successful one, there are numerous more that have faltered in the long run. There can be a lot of reasons for failure like a bad economic model, poor execution, lack of investment and most importantly choosing the wrong market. There are some markets where an online marketplace (or intermediary) creates value while somewhere it does not.

Before jumping in and start building a digital B2B business, it is better to look through some factors that affect the success of one. There are numerous resources to read about it but Bill Gurley’s 2012 article “All markets are not created equal” is still probably the best starting point. There are quite a few things to think through before building a marketplace, we have listed down some of the important ones for a B2B marketplace

Use of technology- First and foremost it is important to understand, what is the value technology can bring to this supply chain: Is it discovery? (increasing the number of buyers and sellers), is it user experience? (better workflows) or efficiency? (intelligent matchmaking). Also, marketplaces tend to be side oriented i.e. will solve the key problem(s) on either one of supply or demand, think through where is the bigger pain point to be solved using technology.

Fragmentation- This is one of the most important factors to consider before jumping in with a marketplace. The biggest problem that a marketplace solves is discovery and transaction facilitation (by inducing trust), this is what creates value for the intermediary. In the case of supply and demand concentration, this value tends to diminish very quickly. All other things remaining equal, High fragmentation in buyers and suppliers is positive for the marketplace. High concentration on both sides, practically renders a marketplace (or intermediary) redundant. If you have to look at a market with a concentration on one side, it is usually better to build in markets where supply is fragmented.

Throughput- It is important to look at what is going to be the Average order value in the supply chain and also what is the frequency of transactions. A high AOV enables the marketplace to grow faster. A high-frequency marketplace tends to be stickier with high recall value and so (generally) higher cost of shifting. Ultimately, the average transaction value, frequency, and margins (take rate) define the long-term economic viability of the marketplace. It’s important to remember that in B2B, more often than not, margins are lower than in B2C, on a per-transaction basis the unit economics (most of the time) makes sense if the average transaction value is high.

Value chain margins- A key difference between consumer and B2B markets is that the inherent motivation for a business to transact is economic rather than consumption, this makes the value extraction by the marketplace to be mostly dependent on (and capped to) the overall value chain margins. Given that one of the key lures for the participants (supply and demand) is going to be an economic advantage, the take rate will be a smaller piece of the value chain margin. Interestingly, there are cases where the value chain margin is not rigid but expandable, in cases where capacity utilization/inventory liquidation/ ‘sweating the asset’ is important, dynamic pricing can unlock better margins.

Commodity v/s specialized product- An online marketplace usually brings in value of discovery and trust between the transacting parties. In the case of a commoditized or branded product, trust is not that big an issue, in such cases, generally, margins tend to be much lower than specialized/custom products/services.

Direct v/s Indirect- Whether the underlying product/service is direct (eg-raw material) or indirect (eg stationary) expense, defines the underlying motivation for the customer. For a direct spend, price becomes a top priority along with the expectation of zero failure rate in fulfilment. Inertia to change vendors is high in this case which results in lower take rates and longer sales cycles. If successfully executed, direct spending provides a recurring, predictable, and sticky business to a marketplace. For indirect spends, take rates can be higher but the barrier to replacement for the marketplace is comparatively lower.

Monetization and business model- Depending on the value chain margins and overall marketplace dynamics, the business models can go from an open marketplace to a managed marketplace. Similarly, the monetization at scale can be through transaction take rate, subscriptions/advertising, or ancillary services (logistics, credit).

Network effects/Moats- Typically open marketplaces have strong network effects and moats. For managed marketplaces specific workflows, data, and allied services can help create effective structural moats.

To summarize, it’s critical to choose the right market and business model before diving in to build a B2B marketplace. The marketplace for a custom/specialized product in a highly fragmented market has a better chance of success compared to a marketplace in a highly concentrated market with a standard product. Also in B2B specifically, it’s critical to think through how you can acquire, onboard, and manage the customers and suppliers efficiently. Because of higher-order values and the criticality of transactions, the zero human touch model is difficult to succeed (at least in the initial days). Business workflows, decision-making, and payment terms are also not simple and straightforward, one of the big challenges that the B2B marketplaces have to navigate (which their consumer siblings don’t) is managing collections, working capital, and credit. It is critical to keep it on a tight leash and put-in processes to skip the downward spiral of the cash trap.

We at Kae Capital continue to be very bullish on B2B commerce and are early investors in Zetwerk, 1K, and a vertical B2B e-commerce marketplace (to be announced soon). If you are building something in B2B, give us a shout atgaurav@kae-capital.com

India has 22 official languages, excluding English, each of which has millions of speakers.

88 percent of Indians can’t speak English (let alone read it), yet when you look at the languages on the internet in India, it’s only in English.

Hindi is used by less than 0.05 percent of websites on the internet, Bengali by less than 0.018 percent, Tamil by less than 0.007 percent, and so on. I hope you get the drift.

I have thrown a lot of numbers up till now, but the ultimate point is this:

99.9 percent of the internet is in languages 90 percent of Indians don’t understand. Is it possible to make a “Digital India” without changing the language of the internet?

Far from infinite, the internet seems to be only as big as the languages you speak. For a non-English Bengali, it is just a few government sites, news sites, apps, and movies on Youtube. However, a couple of new-generation startups have started their local language versions.

I tried living in this pond for the last week and the experience has been highly frustrating. I changed my Android system setting to Hindi (as that’s the only other language I know), changed my Keyboard to Google Indic Keyboard, and tried avoiding all English content that was thrown at me.

Here are a few things I realized in this eye-opening exercise:

No SwiftKey for Hindi. This is the first thing I realized. (I also realized how much I’ve taken SwiftKey for granted in my life.)

Content creation in English is indeed 90 percent faster than in Hindi.

There’s no camera app for Hindi. I can’t use the filters and lenses on Instagram or Snapchat without bumping into English roadblocks

A lot of apps that I took for granted don’t exist for vernacular users. Zomato and Swiggy don’t exist in this small pond.

I can do google searches, but the results in Hindi are very limited, and no meaningful information comes out of them.

Let us now look at some of the most in-demand digital categories and how vernacular is faring in our most popular startups’ priorities.

Neither Flipkart nor Amazon offers multi-lingual support at the moment. Even companies in the long tail of commerce such as Shopclues and Craftsvilla are currently only available in English.

Paytm does allow for multi-lingual support upon changing the language of the phone but only for certain sections of the website.

Travel and transport

In the cab-hailing space, while Ola doesn’t support multiple languages, Uber does change its interface based on the mobile OS setting (Android in my case).

In the travel space, both Makemytrip and ixigo have their train apps in multiple languages. However, both their main apps are still only in English. I couldn’t find any other travel app which supported any Indian language. Even IRCTC’s official mobile app didn’t. (Their website does support Hindi though.)

Leisure and entertainment

This is a category in which vernacular users do have some relief, not because of any Indian startup, but because of two apps: WhatsApp and Facebook.

Whatsapp is available in about 10 Indian languages; it changes depending on the language of your phone. (It also has a crowdsourcing platform for its language translations.) Facebook, similarly, changes languages depending on your phone and is available in 12 regional languages.

Apart from these two, back home, Bookmyshow offers support for five Indian languages.

Very recently, apps like Sharechat and Pratilipi are trying to tap the same market, but there’s yet to be a verdict on these apps.

News

This is probably the only category where certain standalone players have made it big (or at least seem to). While Facebook and Whatsapp do tend to provide the daily dose of content, more organized news apps like DailyHunt and UC News are also getting a lot of love from vernacular users (both sites with more than 10 million downloads on PlayStore).

Very recently, InShorts has also started with Hindi news. Most of the offline newspaper companies also have vernacular websites which get millions of hits themselves.

Of all the segments, news seems like the only segment where the needs of vernacular users haven’t been ignored completely — although there’s still a lot to yearn for.

Games

Candy Crush and Subway Surfers seem to have the same addictive effect on vernacular users as on English users. There have also been a few other games made specifically for Indian tastes like variants of Teen Patti and Chhota Bheem but the vernacular aspect is still missing.

While vernacular users still get a steady supply of casual games, there are virtually no serious or strategy-type games in the market for them.

Challenges

There is a multitude of challenges that this digital language divide possesses; the opinions of Vernacular users are not expressed on the internet. Digital Language Death researcher Andras Kornai claims that 95 percent of all languages in use today will never gain traction online. According to him, it is a real danger that new users, influenced by the volume of content in dominant languages, will abandon their mother tongues online. This seems to be happening to a lot of vernacular users already.

In 2011, the UN declared access to the internet as a basic human right. However, it seems like it is only dominated by a certain elite. On the internet, dominant languages are amplified and end up largely speaking for those with less powerful voices.

But is it possible to bridge this digital language divide? There are quite a few arguments against it.

Bi-lingual users, who can understand English partially, will always prefer the internet in English because of its vast reach.

However, China has a lot of platforms specifically built for Mandarin. They have been able to make their own versions of Google, Facebook, Twitter, and Youtube primarily because less than 1 percent of their population speaks English (this number stands at more than 10 percent in India). Because many Indians aspire to speak English, it is virtually impossible to create separate vernacular platforms.

Another argument on this is that vernacular consumers are not monetizable. Very recently, Mohit Bhatnagar of Sequoia Capital put forward excellent data points countering this myth.

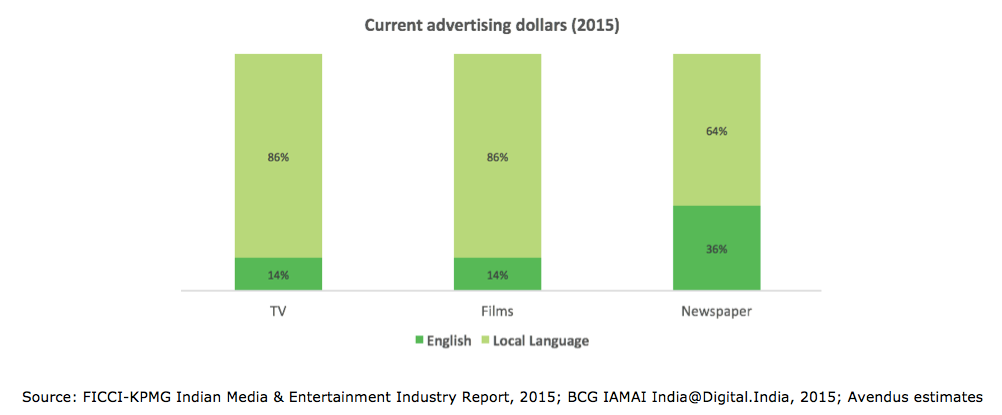

It is clear that advertisers have found local language consumers to be a better TG in the offline space (TV, films, and newspapers).

While the share of local language on advertising spend is 86 percent for TV, 86 percent for films, and 64 percent for newspapers, it is only 5 percent on digital.

Opportunities

In a recent talk, Kevin Bharti Mittal pointed out that while the media talks about hundreds of millions of mobile internet users in India, in fact, we have no more than 90 million.

With data becoming cheaper, many proclaim that new users will come on board. I think it will be virtually impossible for them to do this unless full-fledged, self-serving native language apps are provided. Technology and mobile apps will always remain an alien concept to them until it becomes something they understand.

DoT has already made it mandatory to have local language support in smartphones from July 2017 onward. Companies like Google (with its Indian Language Internet Alliance) are paving the way by making Indic Keyboard, local language fonts, and Unicode standard to provide the base for content creation and discovery.

Here are a few ideas that come to mind:

Needs

Improve business productivity: There is a pent-up demand for bridging the regional language information asymmetry in agriculture and farming. Millions of Whatsapp communities also point towards a need for organized channels for promoting trade in vernacular.

Banking and payment services: The success of MFIs is not just with rural but urban consumers as well. This clearly shows the potential and demand for banking solutions. Current strides towards a cashless economy provide the perfect launchpad for the next wave of banking and payment solutions to be in vernacular. Last-mile banking solutions are also set to be disrupted.

Employment: English has become almost a prerequisite for employability in India. The National Skill Development Council has recognized it as an essential skill to complement over half of 21 core skills. A plethora of opportunities lie in vocational training, employee training, and employment; the same portals that brought jobs to English speakers over the last two decades won’t suffice the unique needs of this section.

Education: Given the digital divide and the aspirational nature of English, learning this language has become a no-brainer opportunity. While Indian English users have multiple online platforms, local language learners have to rely on just physical books for their learning needs. The waves of personalization and interactivity disrupting education are yet to reach regional language learners.

Wants

Entertainment

Various content players have started creating video content in Hindi, but not so much for other regional languages.

Ecommerce

Vernacular reviews-based, social, and curated shopping networks, which aggregate all e-commerce products and their reviews.

Audio/video-based assisted e-commerce

Content Creation

Camera apps that allow users to associate their favourite film/TV content with their images/videos. Dubsmash does allow for something similar with videos but much more innovations seem possible.

Keyboards that allow for easier Indian language input. Initiatives like IIT Bombay IDC’s Swarachakra seem to be a step in this direction.

All I’ve mentioned above could become opportunities for new-age startups to tap. It is time we saw platforms built for Indian languages.

If typing in Hindi is harder, it is time we make it 100 times easier by using images, audio, or video to communicate (or making an easier keyboard itself). If no good Bengali fonts exist, let’s make them. If no Telugu camera apps exist, let’s make one which puts global players to shame.

The timing can’t be better than this. Smartphone sales are at all-time highs and data prices are getting cheaper by the day. We literally are left with no excuses.

The facts and opinions mentioned above hold true as of December 13, 2016.