Why India’s Personal Concierge Moment Is Finally Here and Why It’s Harder Than It Looks

At some point recently, you probably tried to get a restaurant reservation at Pizza 4P’s in Bangalore for Saturday, only to realise everything was already booked out. Or you have been meaning to renew your car insurance, but it keeps slipping down the to-do list. Maybe you need to find someone to frame your painting, sort out your meal plan for the week and instruct your house help on what to pack for lunch, or have your visa form filled and documents organised. And then there are the small but urgent tasks like booking a driver for the airport at 5am. The mental load of managing life’s long tail of tasks is very real, and it compounds quietly.

India is building a fix for exactly this. And it is moving fast. We are watching a new category take shape in real time: personal concierge services, the idea that a single platform, a single chat window, or a single person can absorb all those loose threads of your day and get them done. No more tab-switching, no more no-show vendors, no more cognitive drain over things that really should not require this much energy.

As a consumer, I would love my own PA (and who wouldn’t). As an investor, I am asking whether this is the next big thing or the next cautionary tale. The answer, as with most things worth building, sits somewhere in the messy middle.

Over the past decade, Indian consumers have been steadily conditioned to expect speed, reliability, and immediacy. In urban India, time is increasingly valued more than money. The real question now is how far up the value chain this expectation will travel.

India’s ~$60Bn home services market (FY25) is growing at 10-11% CAGR through FY30, with <1% online penetration. Concierge platforms sit one layer above this market, coordinating not just home services but the broader long tail of everyday tasks.

What Exactly Is a Personal Concierge Platform?

At its core, a personal concierge service is an interface, human, AI, or hybrid, through which you delegate tasks that are too small to hire someone full-time for, but too annoying and time consuming to do yourself. It handles the “long tail” of life admin.

The four underlying actions are consistent across every platform in this space: research, coordinate and communicate, book and negotiate, and handle routine/recurring tasks. The surface area of a working urban Indian household is surprisingly large: supplies, government tasks, kids, parents, vehicles, bills, staff coordination, kitchen, appliances, health, and pets. Without an assistant, you end up being one. The question every concierge platform is wrestling with is how much of that universe to take on, and in what order.

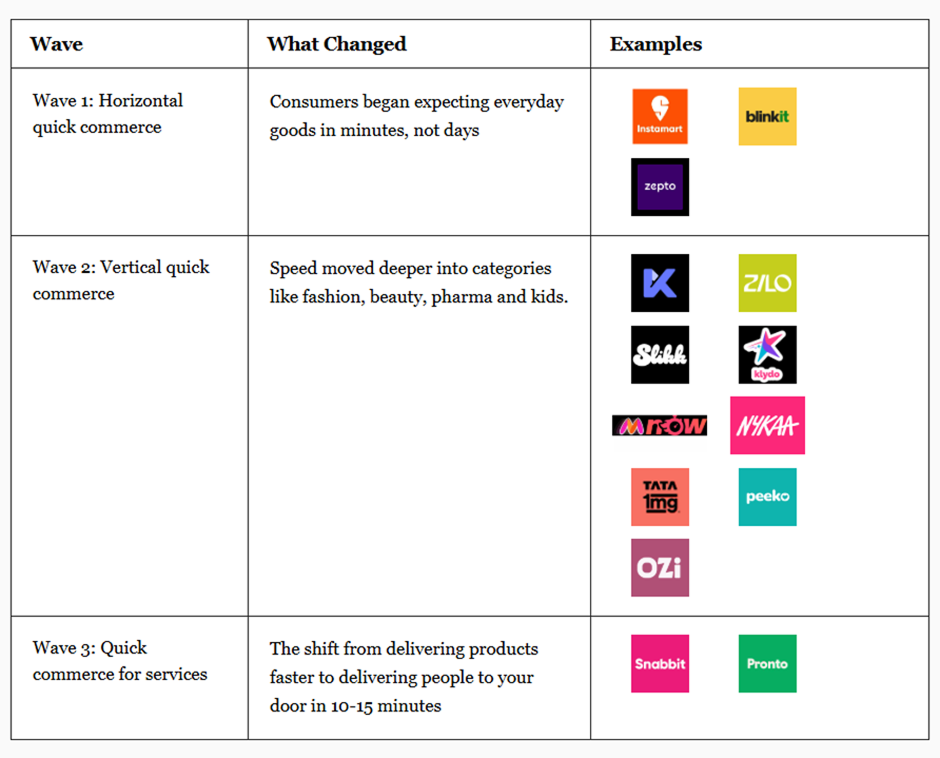

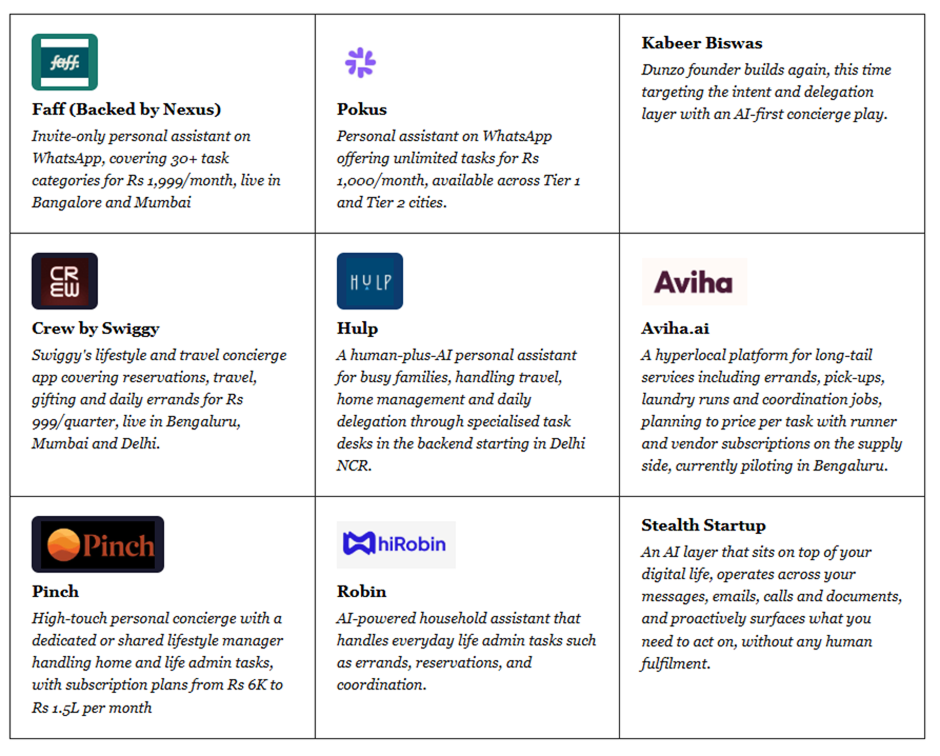

The Players Building This Category Right Now

India’s concierge startup landscape is seeing multiple experiments, each testing a different model for delegating the long tail of life admin.

Why Didn’t This Work Before?

Between 2014 and 2015, a barrage of home-services startups launched including LocalOye, TaskBob, Zimmber, Housejoy, Mr. Right. Most had shut down by 2017. Why?

The first reason was premature copying of the US on-demand model. American consumers have a long history of paying for home services through formal channels. In India, that behaviour was far less established, and adoption outside the early-adopter bubble was slow.

The second reason was unit economics. Customer acquisition cost was high, and when funding tightened in 2016-17, companies without a clear path struggled to survive and folded quickly. Urban Company (then UrbanClap) reported losses nearly Rs 60 crore on a revenue of mere Rs 2.8 crore for FY16, with CAC of Rs 300-400. However, the company had raised ~$57 Mn by 2017 (Total Funding raised ~376 Mn) giving it the capital runway to absorb losses that competitors could not.

The third reason was quality of service. Many early players such as LocalOye, Housejoy and Zimmber operated lead-generation marketplaces: surface a service professional, collect a lead fee, and leave the outcome largely outside the platform’s control. In practice, this was not meaningfully different from platforms like JustDial.

Urban Company took a different approach, investing heavily in training, standardisation and supply quality, effectively building a full-stack services business rather than just a discovery platform. This approach was slower and more expensive, but it improved service quality, drove repeat usage, and gradually made the economics work. By FY25, the company had scaled to Rs 1,144 crore in revenue with Rs 28.5 crore PBT, 6.8 million annual transacting users, and NTV of Rs 3,271 crore.

What has changed in 2024?

Three things, and they are significant.

First, AI has matured enough to meaningfully understand context, coordinate across tools and APIs, and handle the messy, non-standard tasks that a concierge platform needs to manage. Models like Claude and GPT can now integrate with MCPs and live API environments to actually execute tasks rather than just generate responses. The real leverage comes from building persistent context. A system that continuously learns from your messages, emails, and calls begins to understand what matters to you and can surface actions before you even ask. Over time, that accumulated memory becomes a structural advantage that is extremely difficult to replicate and creates stickiness. This does not eliminate the role of humans entirely, but it dramatically reduces the need for constant human intervention. In effect, the platform stops being a tool you query and starts becoming one that simply knows how your life operates.

Second, India’s digital infrastructure is now dense in ways it was not in 2015. UPI handles payments, hyperlocal logistics networks handle physical errands, and e-commerce APIs handle ordering and returns. The orchestration layer finally has something to orchestrate.

Third, and most importantly, Indian consumers have been trained. Ten years of Swiggy, Blinkit, Ola, BookMyShow, Urban Company: a generation of urban professionals knows what digital convenience feels like and is willing to pay for it. The 3 million Zomato Gold members (Q2FY24), the 65 million Amazon Prime subscribers (Jan’26) and the 5.3 million Swiggy One members (FY24) paying for convenience are proxies for a consumer already in the mindset of subscribing to make life easier.

What This Space Still Has to Prove

Will People Actually Change Behaviour?

The addressable pool is not the constraint. The harder question is behavioural: what share of them will actually delegate, pay before they have experienced the value, and trust a platform with the intimate logistics of their home and family? Convenience adoption in India has historically required a forcing function. Swiggy and Zomato worked because hunger is daily and urgent. Uber worked because autos were unreliable. The concierge proposition asks consumers to develop a new habit without an obvious daily trigger. That is a different and harder ask. The open question is whether adoption follows, or whether this remains a product that urban professionals admire but never quite get around to using.

Can You Stand for Everything Without Standing for Nothing?

The breadth of the concierge proposition is also its biggest marketing liability. When your product does everything, you can end up owning nothing in the consumer’s mind. The counter-argument: task diversity, from meal planning to customer support follow-ups, keeps the platform top of mind, which drives further usage, which builds dependability. The risk is not breadth per se, it is breadth without reliable execution.

Subscription or Pay-Per-Task: Which Model Wins?

Pay-per-task is the easier entry point. The value is immediate and tangible. The problem is that it does not build habit. Customers come when they have a task, disappear when they do not, and may never develop the reflex to delegate.

Subscription solves for habit but creates a harder upfront ask in India where consumers are reluctant to commit before they have experienced the value. The platforms that crack it will price it low enough that signing up feels like a no-brainer, then let autopay eliminate the friction of renewal. The real mechanism kicks in after: once someone has paid for a month, they look for reasons to use it. Habit forms not because the product trained them but because the sunk cost nudged them. Low enough to acquire, sticky enough to retain.

The holy grail is when that reflex becomes anticipation. A platform that builds enough context about your life to act before you ask. The anniversary dinner already reserved. The cab already booked. When a platform gets there, retention stops being a sales problem and becomes a product property.

Can You Actually Own Every Outcome?

JustDial’s limitation was never discovery. It was accountability. It surfaced vendors but created no ownership of the outcome. A concierge platform that manages the relationship, tracks quality, and stands behind the result is a fundamentally different product. That accountability is the moat. It is also the hard part.

Urban Company earned it by doing something operationally brutal: training, standardisation, and supply quality across a defined set of skilled and semi-skilled services. It works because a bathroom deep-clean or an AC repair can be broken down into repeatable steps. You can write an SOP. You can train to it. You can measure it. A concierge platform does not have that luxury. The task surface is effectively infinite, and the tasks are nothing like each other. Cleaning a carpet and filling a US visa form are both valid requests. They require different expertise, different vendor relationships, and completely different definitions of done. The accountability promise gets exponentially harder to keep as the task list grows. And the task list is the whole point.

The Unit Economics Challenge Nobody Talks About Enough

The operational cost structure of a human-in-the-loop concierge is heavy from day one. Relationship managers, coordinators, task executors: the overhead arrives before the revenue does. Then there is CAC. You are selling a habit change to a sceptical consumer who has never delegated before. That means performance marketing to find them, brand building to convince them, trials and handholding to convert them, and a subsidised first experience to keep them. Price it low enough to acquire and you bleed on every early customer. Price it at full value and nobody signs up. Then compound that with churn. A customer who subscribes, uses it twice, and quietly cancels has cost you acquisition, onboarding, and service delivery. You have recovered nothing. The unit economics only work if retention is strong, usage is high, and automation progressively takes over the repetitive tasks. Three things that all have to go right simultaneously, in a category that is still figuring out the product.

Who Is the Real Customer Here?

The natural early adopter is not the household with a driver, butler, and full time cook. That problem is already solved with staff. The more interesting customer is the Rs 25L+ urban professional with a part-time bai who still manages the forty small things that fall between the cracks. Time-poor, but not staff-rich.

The key question is how often this customer will actually delegate and what they will be willing to pay before experiencing the value. There is also a structural constraint. Below a certain income level, the willingness to pay for delegation is limited. Above a certain level, the problem is already staffed away.The addressable band in the middle is real. Whether it is large enough to build a meaningful business remains the open question.

What I Am Watching as an Investor

The concierge space is genuinely exciting but genuinely hard. Here is what I would be tracking:

- First-task success rate: The single most predictive metric for retention. Nail the first few tasks and habit starts to form. One failure in the first few weeks and it is very difficult to recover the relationship.

- Monthly active delegation rate: Subscription revenue without recurring task delegation is just deferred churn.

- The automation ratio: How quickly are players moving toward meaningful automation of objective tasks? This is the primary driver of unit economics improvement.

- Vendor quality and SOP depth: Technology is the visible layer. Operations is the defensible layer: a curated vendor list, task SOPs, and consistent quality checks at every step. Urban Company spent years building this. The new wave needs a shortcut via AI.

- The AI memory layer: Whoever builds persistent context, the platform that actually knows what you need before you ask, has a structural advantage that is very hard to replicate. That memory is the subscription that never gets cancelled.

- Capital access: This is a capital-intensive business with a slow habit formation curve. The companies that survive will be those that can repeatedly raise capital and fund the operational build-out required to reach scale.

- Unit economics over time: Early economics will look messy. The real question is whether CAC, fulfilment costs, and operational overhead improve meaningfully as usage deepens and automation increases.

- Founder heuristics: In a category with no established playbook, the rules founders choose to operate by matter enormously. How aggressively they automate, how narrowly they define the task surface, how they execute and how they build trust with users will shape both the product and the economics.

The Bottom Line

India’s personal concierge moment is real. The consumer behaviour is there. The AI infrastructure finally exists. The willingness to pay for convenience is demonstrated at scale across quick commerce, food delivery, and streaming subscriptions.

But the graveyard of 2014-15 is not ancient history. It is a reminder that a real problem and a willing consumer are necessary but not sufficient. What killed the last wave was not a lack of demand. It was unit economics that did not work, quality that could not scale, and a habit that never fully formed.

The players who will win this time are the ones who resist the temptation to own everything before they have earned the right to own anything, pick the micro-cluster, nail the first task, build the vendor depth that makes accountability real and then build the memory layer that turns a transaction into a relationship.

The concierge category’s true unlock comes when the platform moves from reactive to proactive: when your assistant books the restaurant before you remember it is your anniversary, replenishes your supplements before you run out, and has your car service scheduled before you notice the 10,000 km mark. When that happens, the PA you never had becomes the subscription you never cancel.

Whether this wave of builders gets it right before the economics run out is, as always, a question only time can answer.